Base Metals

And then reality hit: Iron ore and downside risk

The market has earnings at Rio Tinto (ASX:RIO) and BHP (ASX:BHP) crashing 48% and 28%, respectively, for the six months … Read More

The post And then…

Okay. Chinese household savings might have cracked a feverishly high 17.9 trillion yuan (circa US$2.6 trillion) over the last year, but even a torrent of domestic spending is unlikely to provide any sustaining spark to a dampened Australian iron ore sector.

After a bit of a 2023 China re-opening soiree – which lasted through January across the local commodities sector – CBA is calling in the cleaners and the biggie iron ore producers look like the first to be shown the door.

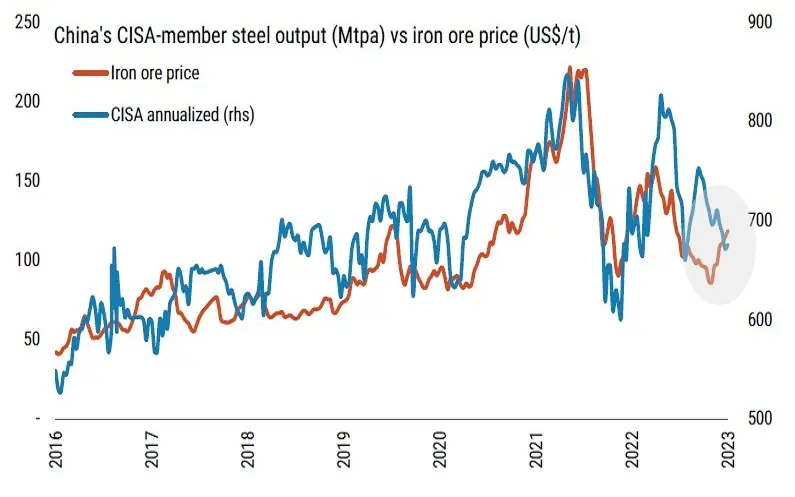

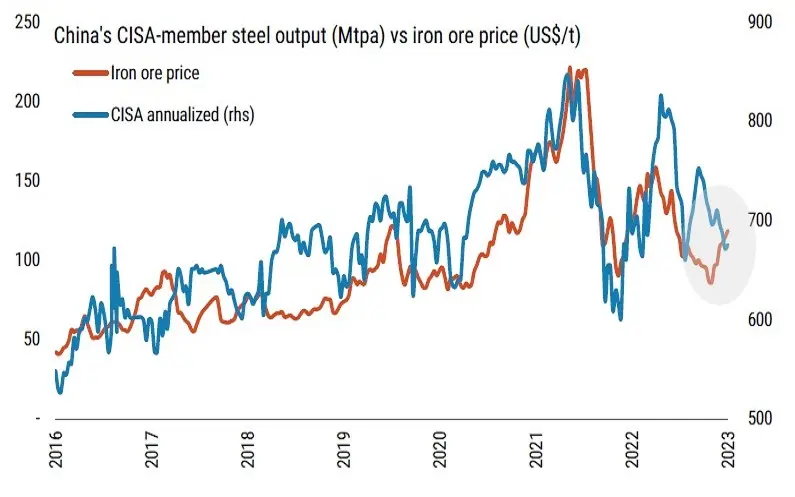

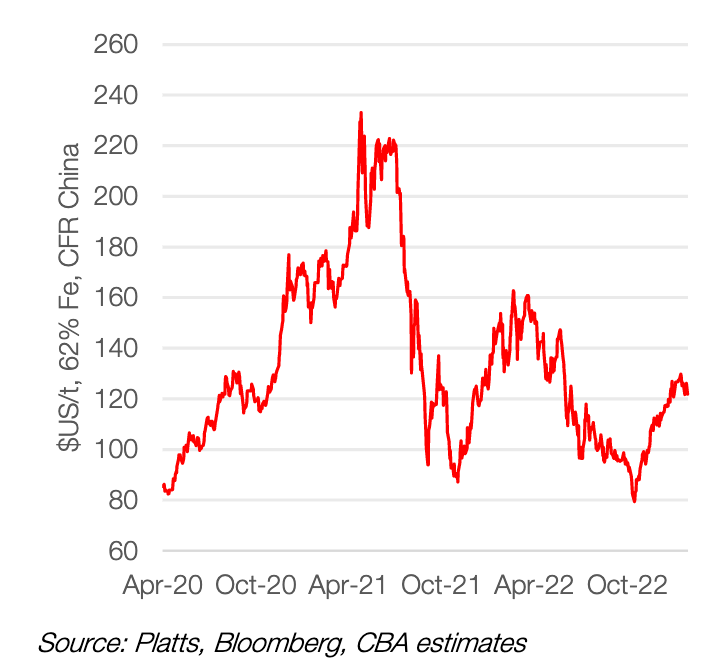

The bank’s commodities research crew says the outlook isn’t grand. Since hitting a low of $US80/t (62% Fe, CFR China) in late October 2022, our local producers lifted in line with a decent iron ore price upswing.

Josh Chiat is all over this – minus the waffling – in his latest.

For now, I’m telling you there’s some cray-cray mixed signals and at $US120-130 a tonne, all the happy-happy, joy-joy signals we’ve been getting out of a re-emerging Beijing, aren’t the whole picture.

Morgan Stanley disagree. They sees all kinds of upside for iron ore, with Brazilian production getting rained out and some US$4 billion of pandemic-postponed infrastructure waiting on the sidelines. They’re forecasting a price of US$140 a big pop by the 2H this year and reckon it’s a China-led recovery all the way, but I’d want to hear out Vivek Dhar at CBA and his team.

Safe as houses

Since early January, we’ve been sitting at this comfy spot. In parallel, China’s households have been pinching pennies, with annual savings up 80% from 2021, according to the People’s Bank of China (PBoC) last week.

That’s more than one third of Chinese households’ total income. Way yonder in another world (ie: before the pandemic), the ordinary Chinese punter looked to stow away about a fifth of their income.

While an upbeat circle of economists led by Goldman Sachs sees a strong Chinese consumption-led recovery, UBS believes that the spend fervour of this pent up demand will in fact be fairly cautious with local consumer confidence severely dented after the trauma of the last 12 months.

UBS puts China’s total household ‘excess savings’ at 4-4.6 trillion yuan (between US$590 billion to US$680 billion).

The Swiss bank says that the zip in the Chinese consumer won’t return until both employment and household incomes firm after a punishing pandemic.

So what happens with that money is a major question for analysts, and at the core of it is China’s rattled property sector and at the core of that is our iron ore sector.

Our own problems

The Aussie majors have their own challenges at home to negotiate before they consider life post-China’s COVID lockdown. The big mining stocks have traded sideways this week as iron ore prices continue to hold, but for how long? on Tuesday, Rio Tinto fell 0.46% to $121.74, BHP fell 0.31% to $47.72, while Fortescue gained 0.14% to $22.17.

The miners are expected to offer a mixed bag of forward guidance this year, with the uncertainty, shape and nature of China’s post-pandemic economic recovery.

Rio Tinto, BHP Group and Fortescue are all facing a torrid earnings season with earnings ready to finally break off their record highs.

According to estimates from Vuma Financial, the majors are set to deliver a major earnings disappointment for the six months to December.

The market has earnings at Rio Tinto (ASX:RIO) and BHP (ASX:BHP) crashing 48% and 28%, respectively, for the six months to December 2022.

Fortescue’s half-year is looking a little less catastrophic but a 16% slide on this time last year won’t win Twiggy the praise, nor the profit he’s been enjoying throughout a happy pandemic.

After massive returns to shareholders and Twiggy, this year is going to see a rejig in dividends, with lower revenues squeezing dividends.

But FMG is far from sitting pretty. At the beginning of the month Goldman Sachs reiterated its sell rating on Fortescue, with a measly $13.60 price target.

That’s a potential downside of around 40% over the next 12 months.

CBA: Iron ore price rally unlikely to remain sustainable through 2023

China’s iron ore demand is the major driver of spot iron ore prices given that China accounts for 65-70% of the world’s iron ore imports.

According to Vivek Dhar, CBA’s director of mining and energy commodities research, the re-opening of China’s economy has placed the world’s second largest economy back in play as an outlying engine for not just our economic growth, but as a driver of growth across other major economies.

“The composition of China’s economic growth matters,” Vivek says.

“China’s steel intensive economy mainly comprises of construction, manufacturing & machinery as well as the auto sector. Construction is the most important sector given it accounts for 60-65% of China’s steel demand.

“Construction can be broken down further into the sub-sectors of property and infrastructure. Property and infrastructure account for 35-40% and 20-25% of China’s steel consumption respectively.

Iron ore spots – $US/t, 62%Fe, CFR China, daily

The welcome lifting of China’s calamitous zero-COVID policy back in early December removed a significant constraint on China’s economy, CBA’s economics team says, with Beijing now concentrating its focus from COVID-control to economic growth.

CBA has forecast China’s economy will grow 5.5% in 2023, almost double its 3% of last year.

China GDP 2023, CBA

This means a change of tune for domestic infrastructure-related steel demand, with policymakers looking to stimulate through local infrastructure projects which in turn is expected to accelerate demand this year.

China dominates the global iron ore stage because its dodgy property sector, ongoing infrastructure scale-up, and ye olde heavy-manufacturing. It’s still soaking up some 71% of global iron ore demand.

According to CBA, China’s steel demand rose by somewhere between 2.5-5% in 2022.

Vivek says the key indicator to watch is the pick-up in China’s issuance of local government special bonds.

“These bonds are used primarily to fund infrastructure projects. China’s issuance of local government special bonds rose by 4.2% last year and is expected to lift even higher in 2023.

“We’ll get a better of understanding of how strongly China’s infrastructure sector will grow at China’s ‘Two Sessions’ next month. Policymakers typically set economic targets, including the quota for China’s local government special bonds, at the ‘Two Sessions’.”

Any growth in China’s steel demand from a boost in infrastructure construction is likely to be offset by another contraction in China’s property construction this year, Vivek warns.

“New housing starts is the key indicator to watch for steel demand from China’s property construction sector. New housing starts (measured in floor space) plummeted ~40% in 2022 and is likely to remain in contractionary territory in 2023.”

On that note, Fitch Ratings has the drop on how much action the local concumer saw over the mos recent lunar New Year holiday. Really, China’s first in a good few years.

High-frequency consumption data during the Chinese New Year holidays suggest a decent start to consumption recovery in 2023. High-end and mid- to high-end discretionary service sectors will outperform. https://t.co/Bm8b7aitPX#china #chinaeconomy #chinabusiness #asiapacific pic.twitter.com/vN3BOY2g76

— Fitch Ratings (@FitchRatings) February 7, 2023

Vivek says the rate of China’s property contraction is likely to ease through this year.

That’s a signal “that the worst is likely over for China’s property-related steel demand.”

Back on point

“Policymakers have looked to ease credit conditions for China’s property developers,” Vivek says, pointing to China’s 16-point property rescue package of late last year which shows how Beijing is back to backing the errant property sector.

“It is still anticipated though that steel demand from China’s property construction sector will contract notably again in 2023. And the extent of contraction is expected to be steep enough to bring down China’s total steel demand by 0-2% in 2023.

“Weaker Chinese steel demand should weigh on China’s steel output and iron ore consumption. We think weaker Chinese iron ore demand, combined with a modest uplift in seaborne iron ore supply will weigh on iron ore prices through 2023.

“We think prices will drift lower to $US100/t in coming months.”

The post And then reality hit: Iron ore and downside risk appeared first on Stockhead.

White House Prepares For “Serious Scrutiny” Of Nippon-US Steel Deal

White House Prepares For "Serious Scrutiny" Of Nippon-US Steel Deal

National Economic Adviser Lael Brainard published a statement Thursday…

How to Apply for FAFSA

Students and families will see a redesigned FAFSA this year. Here’s how to fill it out.

Dolly Varden consolidates Big Bulk copper-gold porphyry by acquiring southern-portion claims – Richard Mills

2023.12.22

Dolly Varden Silver’s (TSXV:DV, OTCQX:DOLLF) stock price shot up 16 cents for a gain of 20% Thursday, after announcing a consolidation of…