Economics

Hutchins Roundup: Monetary policy transmission, tax cuts, and more

What’s the latest thinking in fiscal and monetary policy? The Hutchins Roundup keeps you informed of the latest research, charts, and speeches. Want…

By Elijah Asdourian, Alexander Conner, Nasiha Salwati, David Wessel

What’s the latest thinking in fiscal and monetary policy? The Hutchins Roundup keeps you informed of the latest research, charts, and speeches. Want to receive the Hutchins Roundup as an email? Sign up here to get it in your inbox every Thursday.

Credit, interest rate channels more important than exchange rates in monetary policy transmission

Using a multi-country panel of output and price data by industry, Sangyup Choi of Yonsei University, Tim Willems of the Bank of England, and Seung Yong Yoo of Yale show that the credit and interest rate channels of monetary policy are the most important. The authors estimate that industries with more tangible assets, higher investment intensity, faster depreciation, and higher labor intensity are more sensitive to monetary policy surprises, consistent with the credit channel of monetary policy having a larger effect on industries with assets that are more difficult to collateralize. The credit channel is amplified during downturns and in nations with shallower financial markets, as predicted by the financial accelerator effect. The authors confirm the traditional interest rate channel through the sensitivity of durable goods producers to monetary policy surprises; output in that sector varies significantly with the current and expected future borrowing costs facing potential customers. They find no evidence for an exchange rate channel of monetary policy, nor a “cost channel,” where firms might pass increased costs of working capital – a production input – to consumers after a monetary policy surprise. The authors did not test the asset price channel of monetary policy.

Goods sector companies and service sector companies use tax cuts differently

With data on American companies’ balance sheets from 1950 to 2006, James Cloyne of UC Davis, Ezgi Kurt of Bentley University, and Paolo Surico of London Business School find that goods-producing firms spend relatively more on capital and wage bills following corporate tax cuts while service sector companies increase dividend payouts. Companies’ spending peaks about two years after the initial cut in tax rates before going back to normal levels after four years, and the increases are significant: goods-producing firms increase investment by 8%, employment by 2%, and wage bills by 4%, and service-sector firms increase dividend payouts by 5%.

Inflation may come down even if real wages increase

While nominal wages have been growing at a higher rate than consistent with the Federal Reserve’s 2% inflation target, real wages remain below the level implied by their pre-COVID trend. Steven B. Kamin of the American Enterprise Institute and John M. Roberts, formerly of the Federal Reserve Board, use a modified version of the Board’s large-scale macro model (FRB/US) to explore how inflation might respond to the evolution of the gap between real wages and their pre-pandemic trend. Notably, the authors find that if workers try to close the wage gap while companies maintain price markups, the likely result is a wage-price spiral where wage growth is passed through to higher prices, which in turn necessitate higher interest rates that increase unemployment. In this scenario, both inflation and unemployment rise sharply, and the wage gap persists. Conversely, if competition erodes markups, increases in real wages can be consistent with disinflation, they find. In particular, if companies’ price markups are a result of strong aggregate demand, then “the disinflationary benefits of reducing demand pressures may be even greater than generally thought,” they say.

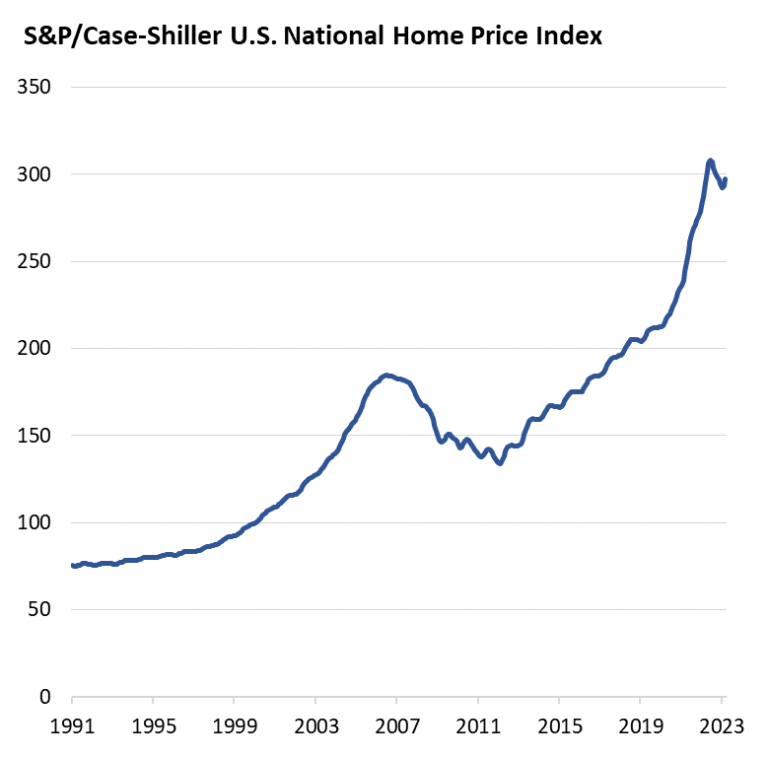

Chart of the week: Case-Shiller home price index has ticked up in recent months

Source: S&P Global

Quote of the week:

“I expect spending and economic growth to remain quite slow over the rest of 2023, due to tight financial conditions, low consumer sentiment, heightened uncertainty, and a decline in household savings that had built up after the onset of the pandemic. Inflation has come down substantially since last summer, but it is still too high, and by some measures progress has been decelerating recently, particularly in the core services sector. While it is reasonable to expect that the recent banking stress events will lead banks to tighten credit standards further, the amount of tightening and the magnitude of the effect such tightening might have on the U.S. economy is not yet clear, and this uncertainty complicates economic forecasts,” says Philip N. Jefferson, Member, Federal Reserve Board.

“Short-term interest rates are 5 percentage points higher than they were a little over a year ago. History shows that monetary policy works with long and variable lags, and that a year is not a long enough period for demand to feel the full effect of higher interest rates. While my base case forecast for the U.S. economy is not a recession, higher interest rates and lower earnings could test the ability of businesses to service debt … Since late last year, the Federal Open Market Committee has slowed the pace of rate hikes as we have approached a stance of monetary policy that will be sufficiently restrictive to return inflation to 2% over time. A decision to hold our policy rate constant at a coming meeting should not be interpreted to mean that we have reached the peak rate for this cycle. Indeed, skipping a rate hike at a coming meeting would allow the Committee to see more data before making decisions about the extent of additional policy firming.”

The Brookings Institution is financed through the support of a diverse array of foundations, corporations, governments, individuals, as well as an endowment. A list of donors can be found in our annual reports published online here. The findings, interpretations, and conclusions in this report are solely those of its author(s) and are not influenced by any donation.

inflation

monetary

markets

reserve

policy

interest rates

monetary policy

Argentina Is One of the Most Regulated Countries in the World

In the coming days and weeks, we can expect further, far‐reaching reform proposals that will go through the Argentine congress.

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

A weird week of macro data – strong jobless claims but…

Fed Pivot: A Blend of Confidence and Folly

Fed Pivot: Charting a New Course in Economic Strategy Dec 22, 2023 Introduction In the dynamic world of economics, the Federal Reserve, the central bank…