Economics

Hutchins Roundup: Neutral rates, missing workers, and more

What’s the latest thinking in fiscal and monetary policy? The Hutchins Roundup keeps you informed of the latest research, charts, and speeches. Want…

By Elijah Asdourian, Alexander Conner, Louise Sheiner, Lorae Stojanovic

What’s the latest thinking in fiscal and monetary policy? The Hutchins Roundup keeps you informed of the latest research, charts, and speeches. Want to receive the Hutchins Roundup as an email? Sign up here to get it in your inbox every Thursday.

Growing supply of government debt modestly increased neutral rates

Long-run neutral interest rates rose after the global financial crisis and during the pandemic, find Thiago Ferreira and Carolyn Davin of the Federal Reserve Board. Using a structural model of advanced economies, they estimate that from 2008 to 2019, neutral rates rose between 0.1 and 0.3 percentage points in the U.S., U.K., Euro area, and Canada. Neutral rates rose faster over the pandemic, with the U.S. and U.K. seeing roughly half-point increases from 2020 to 2022. The growing supply of government debt during the pandemic has exerted the most upward pressure on neutral rates, accounting for almost all the increase. Global financial spillovers and demographics were the most significant drags, although components such as productivity had a larger effect during the pandemic. Overall, these neutral rate estimates fall in the middle of the ranges communicated by the Fed, Bank of England, and European Central Bank, and slightly above the Bank of Canada’s range. The authors note that excluded factors, like heightened uncertainty and trade disruptions from the war in Ukraine, would likely depress neutral rates if they persist.

Estimates of ‘missing workers’ due to pandemic are overstated

Since the onset of the COVID-19 pandemic, the labor force participation rate has declined and payroll employment has fallen below its pre-2020 trend, leading some to argue that the American economy has 5.8 million “missing jobs.” Bart Hobijn of the Federal Reserve Bank of Chicago and Ayşegül Şahin from the University of Texas at Austin argue that most of those jobs are not actually missing, but instead the result of a counterfactual that assumes short-run upward pressure on labor force participation and payroll employment in 2019 would continue through 2022. The authors note that this would have brought the unemployment rate down to 2.3%, which they argue is “unreasonable” and contradicts professional forecasts of the unemployment rate from the months before the pandemic. After accounting for trends in the business cycle, as well as long-term downward trends in both the labor force participation rate and population growth, the authors determine that the number of “missing jobs” that can be attributed to the pandemic is about 810,000.

Pandemic caused a wave of excess retirements

As of October 2022, labor force participation rates were nearly 1½ percentage points below pre-pandemic levels, with an increase in retirees accounting for nearly all the shortfall, according to an analysis of Current Population Survey microdata by Joshua Montes, Christopher Smith, and Juliana Dajon of the Federal Reserve Board. After controlling for pre-pandemic trends, more than half the increases in the retired share of the population are from retirements that would not have happened in absence of the pandemic. Whites, the college-educated, and individuals above age 65 were overrepresented among the excess retirees, which the authors speculate might be due to the larger financial cushion these groups possess. The authors expect that excess retirements will fade into expected retirements “as those who retired early during the pandemic reach ages when they would have normally retired” while the retired share of the population will remain persistently elevated due to demographic trends.

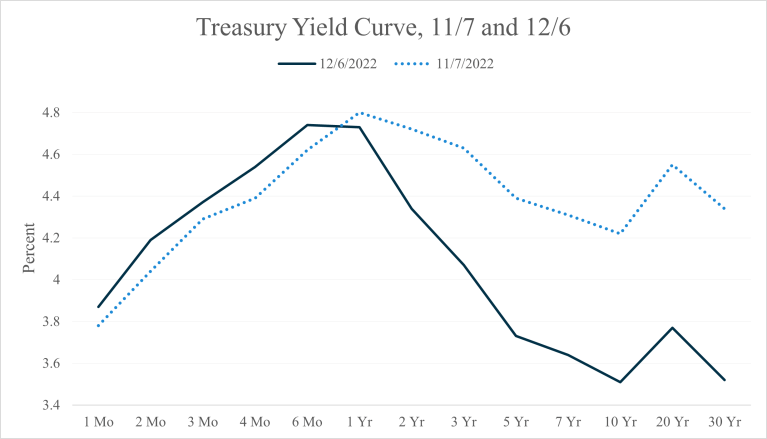

Chart of the week: Yield curve is inverting

Data courtesy of the U.S. Department of the Treasury

Quote of the week:

“Typically, you could expect inflation to get closer to our target with extra time. One reason is that we have raised interest rates already by quite a bit and we’ve said we’ll raise them again. This does not have an immediate effect on inflation, but over the next one or two years those higher interest rates will dampen demand, reduce expenditure, and therefore reduce the ability of firms to charge high prices and in turn limit the scope of unsustainable wage increases. So a basic reason why inflation will be closer to our target is the actions of our monetary policy. We also do think that we will not experience the same energy inflation every year,” says Philip R. Lane, Member of the Executive Board of the European Central Bank.

“But let me also say, we do think there will be a second round of inflation….[M]any sectors need to raise their prices because their costs have gone up. Many workers also have so far suffered a big reduction in their living standards, but we expect them to receive bigger pay increases next year and also in 2024 and 2025. These bigger pay increases will support expenditure and will also raise prices. That is why it will take some time to return to our 2% target. So the second round effects will drive inflation next year and in 2024.”

The Brookings Institution is financed through the support of a diverse array of foundations, corporations, governments, individuals, as well as an endowment. A list of donors can be found in our annual reports published online here. The findings, interpretations, and conclusions in this report are solely those of its author(s) and are not influenced by any donation.

inflation

monetary

reserve

policy

interest rates

fed

central bank

monetary policy

Argentina Is One of the Most Regulated Countries in the World

In the coming days and weeks, we can expect further, far‐reaching reform proposals that will go through the Argentine congress.

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

A weird week of macro data – strong jobless claims but…

Fed Pivot: A Blend of Confidence and Folly

Fed Pivot: Charting a New Course in Economic Strategy Dec 22, 2023 Introduction In the dynamic world of economics, the Federal Reserve, the central bank…