Economics

It’s Not Just Failing Banks: Here Are The Week’s Key Events – CPI, PPI, Retail Sales And An ECB Hike

It’s Not Just Failing Banks: Here Are The Week’s Key Events – CPI, PPI, Retail Sales And An ECB Hike

In case the market "excitement" over…

It’s Not Just Failing Banks: Here Are The Week’s Key Events – CPI, PPI, Retail Sales And An ECB Hike

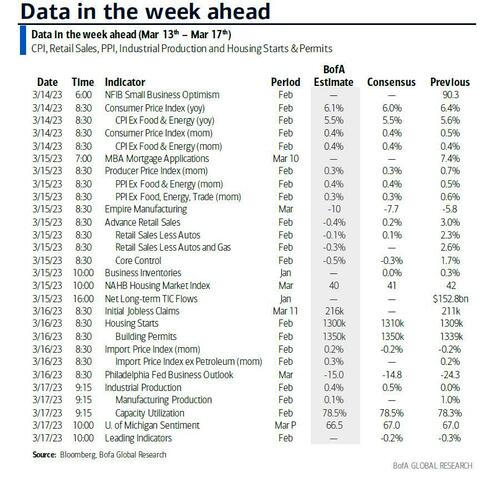

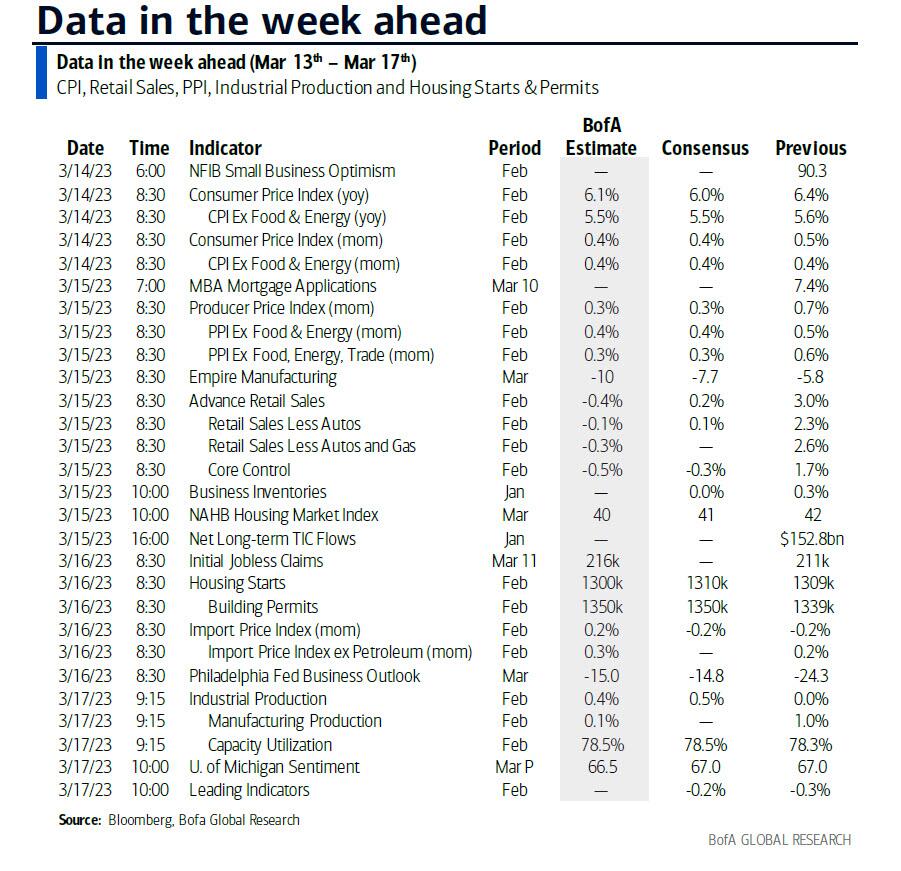

In case the market “excitement” over the past week has not been enough, with the rapidly spreading global bank crisis collapsing rate hike odds and Goldman now calling for a pause in March, tomorrow sees a pivotal US CPI print. As DB’s Jim Reid reminds us, also important will be the ECB meeting on Thursday. In terms of other data, US retail sales (Wednesday), China’s monthly data dump (tomorrow) and various US housing market releases through the week are the highlights. Alas, don’t expect any commentary from the Fed – on these items or the ongoing bank crisis 0 as they are on their pre-FOMC blackout ahead of next Wednesday’s rate decision. According to Reid, “It’s fair to say that the US CPI report tomorrow is not only hotly anticipated but will likely be a swing factor in terms of 25 or 50bps from the Fed next week, alongside the fall-out from SVB.” We disagree, or rather we agree with Goldman: there will be no more rate hikes.

In any case, a quick preview of tomorrow’s CPI from DB economists: they expect headline CPI (+0.37% forecast vs. +0.52% previously) and core CPI (+0.36% vs. +0.42%) will both round to 0.4% mom which is where the consensus is. This will translate to headline dropping 0.4pp to 6% YoY and core down a tenth to 5.5% YoY. They discuss how at the component level, there will be much focus on core goods, as recent disinflationary pressures from used cars and trucks wane.

Retails sales and PPI (both Wednesday) will also factor into the Fed’s 0/25/50bp decision… actually make that -25/0/25bps. For retail sales, after a bumper January, February’s data should see some reversal, as we noted previously. A dip in unit motor vehicle sales will push headline sales (-1.2% vs. +3.0%) lower, while the expected payback from food services and drinking places as well as nonstore retailers should weigh on sales excluding automobiles (-1.1% vs. +2.3%) and retail control (-0.3% vs. +1.7%). For PPI, headline (+0.5% vs. +0.7% mom) will slightly outpace core (+0.4% vs. +0.5%). Rounding out the main US data, investors will also get an array of housing market indicators including the NAHB housing market index (Wednesday) and housing starts and building permits (Thursday).

Turning attention to central banks, the Fed will be in a quiet period until the next FOMC which could be a problem with the banking system suddenly imploding. A key event will be the ECB decision on Thursday. The meeting follows upside surprises from recent inflation readings across the bloc as well as generally stronger-than-expected economic performance. DB’s European economists expect a third consecutive +50bps hike, taking the deposit facility rate to 3.00%, as well as messaging supporting for another +50bps move in May. After that, they see a downshift in June to +25bps, taking the terminal deposit rate to 3.75%. However, they emphasise upside risks to the landing zone of 3.50%-4.00% and do not rule out a terminal above 4%.

Over in the UK, markets will be awaiting the labor market data released tomorrow and the Budget unveiled the next day. For the latter, see a preview from our UK economist here. He expects no large surprises together with a focus on fiscal prudence, with the cost-of-living crisis and public sector services likely the main themes for spending.

In Asia, China’s retail sales and industrial production data tomorrow will be at the forefront of investors’ attention. Current median estimates on Bloomberg are pointing to a strong rebound, with retail sales seen growing 3.5% YTD YoY (vs -0.2% in January) and industrial production forecasted to expand by +2.6% (vs 3.6% in January).

Courtesy of DB’s Jim Reid, here is a day-by-day calendar of events

Monday March 13

- Central banks: BoE’s Dhingra speaks

- Earnings: Porsche

Tuesday March 14

- Data: US February CPI, NFIB small business optimism, UK February jobless claims change, January average weekly earnings, unemployment rate, Italy January industrial production, Canada January manufacturing sales

- Central banks: BoJ minutes of the January meeting, Fed’s Bowman speaks

- Earnings: Volkswagen

Wednesday March 15

- Data: US March NAHB housing market index, Empire manufacturing, February PPI, retail sales, January business inventories, China February retail sales, industrial production, property investment, Japan February trade balance, January core machine orders, Italy Q4 unemployment rate, January general government debt, Germany February wholesale price index, January current account, Eurozone January industrial production, Canada February housing starts, existing home sales

- Earnings: Adobe, BMW, Inditex, Prudential, Ping An

- Other: UK Spring Budget

Thursday March 16

- Data: US March Philadelphia Fed business outlook, New York Fed services business activity, February export and import price index, housing starts, building permits, initial jobless claims, China February new home prices, Japan January capacity utilization, Canada January wholesale trade sales

- Central banks: ECB decision

- Earnings: FedEx, Dollar General, Enel, Rheinmetall

Friday March 17

- Data: US March University of Michigan sentiment, February industrial and manufacturing production, capacity utilization, leading index, UK February BoE/ Ipsos inflation attitudes survey, Japan January tertiary industry index, Italy January trade balance, Eurozone Q4 labour costs, Canada February raw materials and industrial product price

- Earnings: XPeng, Vonovia

* * *

Finally, looking at just the US, Goldman writes that the key economic data releases this week are the CPI report on Tuesday, the retail sales report on Wednesday, and the Philadelphia Fed manufacturing index on Thursday. There are no speaking engagements from Fed officials on monetary policy this week, reflecting the FOMC blackout period. Governor Bowman will deliver a speech on innovation in the banking system on Tuesday.

Monday, March 13

There are no major economic data releases scheduled.

Tuesday, March 14

06:00 AM NFIB small business optimism, February (last 90.3)

08:30 AM CPI (mom), February (GS +0.40%, consensus +0.4%, last +0.5%); Core CPI (mom), February (GS +0.45%, consensus +0.4%, last +0.4%); CPI (yoy), February (GS +6.08%, consensus +6.0%, last +6.4%); Core CPI (yoy), February (GS +5.56%, consensus +5.5%, last +5.6%): We estimate a 0.45% increase in February core CPI (mom sa), which would leave the year-on-year rate unchanged at 5.6%. Our forecast reflects an 8% jump in airfares and another gain in the car insurance category as carriers seek to offset higher repair and replacement costs. We assume a small rise in used car prices (+0.5%, we assume larger increases in the spring) but a modest decline in new car prices (-0.2%) on the back of rebounding incentives. We also forecast a sequentially slower pace of shelter inflation (we estimate rent +0.62% and OER +0.59%) as weakness in new rental pricing begins to offset continued upward pressure on renewing leases. We estimate a 0.40% rise in headline CPI, reflecting stable energy prices and higher food prices.

5:20 PM Fed Governor Bowman speaks: Fed Governor Michelle Bowman will deliver a speech on innovation in the US banking system at an event in Honolulu hosted by the Independent Community Bankers of America association. Text is expected.

Wednesday, March 15

- 08:30 AM Empire State manufacturing survey, March (consensus -8.0, last -5.8)

- 08:30 AM PPI final demand, February (GS +0.2%, consensus +0.3%, last +0.7%); PPI ex-food and energy, February (GS +0.3%, consensus +0.4%, last +0.5%); PPI ex-food, energy, and trade, February (GS +0.2%, consensus +0.3%, last +0.6%): We estimate that the PPI final demand index increased by 0.2% in February. We estimate a 0.3% increase for PPI ex-food and energy and a 0.2% increase for PPI ex-food, energy, and trade.

- 08:30 AM Retail sales, February (GS -0.9%, consensus -0.4%, last +3.0%); Retail sales ex-auto, February (GS -0.7%, consensus -0.1%, last +2.3%) ;Retail sales ex-auto & gas, February (GS -0.8%, consensus -0.3%, last +2.6%); Core retail sales, February (GS -0.4%, consensus -0.3%, last +1.7%): We estimate core retail sales declined 0.4% in February (ex-autos, gasoline, and building materials; mom sa). Our forecast reflects some sequential softness in high-frequency consumer spending data. We estimate a 0.9% decline in headline retail sales, reflecting a pullback in auto sales and restaurant spending and flattish gasoline prices.

- 10:00 AM Business inventories, January (consensus flat, last +0.3%)

- 10:00 AM NAHB housing market index, March (consensus 41, last 42)

Thursday, March 16

- 08:30 AM Housing starts, February (GS +0.2%, consensus +0.1%, last -4.5%); Building permits, February (consensus +0.5%, last +0.1%); We estimate housing starts increased by 0.2% to 1342k in February (vs. a peak of 1,896 in December 2021).

- 08:30 AM Import price index, February (consensus -0.2%, last -0.2%)

- 08:30 AM Initial jobless claims, week ended March 11 (GS 200k, consensus 205k, last 211k); Continuing jobless claims, week ended March 4 (consensus 1,698k, last 1,718k): We estimate that initial jobless claims declined to 200k in the week ended March 11.

- 08:30 AM Philadelphia Fed manufacturing index, March (GS -10.0, consensus -15.0, last -24.3); We estimate that the Philadelphia Fed manufacturing index rebounded 14.3 points to -10 in March, reflecting the reopening of the Chinese economy and sequentially firmer industrial data globally.

Friday, March 17

- 09:15 AM Industrial production, February (GS -0.5%, consensus +0.2%, last flat); Manufacturing production, February (GS flat, consensus -0.2%, last +1.0%); Capacity utilization, February (GS 77.8%, consensus 78.4%, last 78.3%): We estimate industrial production decreased 0.5% in February, reflecting weak auto, oil and gas, and mining production but strong natural gas production. We estimate capacity utilization declined to 77.8%.

- 10:00 AM University of Michigan consumer sentiment, March preliminary (GS 67.5, consensus 67.0, last 67.0); University of Michigan 5-10-year inflation expectations, March preliminary (GS 2.9%, consensus 2.9%, last 2.9%): We expect that the University of Michigan consumer sentiment index rose to 67.5 in the preliminary March report. We expect that the report’s measure of long-term inflation expectations remained unchanged, at 2.9%.

Source: BofA, Goldman, DB

Tyler Durden

Mon, 03/13/2023 – 11:02

dollar

inflation

monetary

markets

policy

mining

fed

monetary policy

Argentina Is One of the Most Regulated Countries in the World

In the coming days and weeks, we can expect further, far‐reaching reform proposals that will go through the Argentine congress.

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

A weird week of macro data – strong jobless claims but…

Fed Pivot: A Blend of Confidence and Folly

Fed Pivot: Charting a New Course in Economic Strategy Dec 22, 2023 Introduction In the dynamic world of economics, the Federal Reserve, the central bank…