Economics

So, Now It’s a June Pause?

Fed officials nod toward a June pause … why economic good news is bad news for the Fed … the market is not a good bargain … C3.ai stock crashes after…

Fed officials nod toward a June pause … why economic good news is bad news for the Fed … the market is not a good bargain … C3.ai stock crashes after not being perfect

First things first, the Senate approved the debt ceiling bill yesterday evening.

The bill now heads to President Joe Biden’s desk where he’ll finally put this matter to rest (until we repeat it all over again in 18 months).

But for now, this cloud no longer overhangs the market, and Wall Street is in party mode. As I write Friday afternoon, all three major indexes are up over 1%. The Dow is up over 2%.

The other major news this morning is the red-hot payroll report. We’ll circle back to those details in a moment. But since it’s part of a broader story, let’s begin a bit further back.

Dance, monkeys! Dance!

In recent days, traders have wildly recalculated their bets on interest rate levels – yet again – after updated comments from various Fed presidents.

For a bit of context, about a month ago, in the wake of dovish commentary from Federal Reserve Chairman Jerome Powell, a rate-pause in June seemed all-but-certain.

As recently as May 10th, Wall Street traders were putting the odds of this June-pause at 95%.

But then came some hotter-than-expected economic data that prompted hawkish Fed commentary.

For example, there was the Fed’s preferred inflation indicator, the Core PCE Index, re-accelerating, coming in higher than forecasts. That resulted in Dallas Federal Reserve President Lorie Logan saying that the economic data don’t justify skipping a rate increase in June.

From Logan:

The data in coming weeks could yet show that it is appropriate to skip a meeting. As of today, though, we aren’t there yet.

Cue Wall Street traders frantically shifting their bets.

As we covered here in the Digest, as of this past Tuesday, that high-conviction of a June-pause had crumpled. Instead, traders were putting majority odds – 60.2% – on another quarter-point rate-hike in June.

But then came Wednesday’s dovish Fed comments from various Fed members.

From Fed Governor Philip Jefferson:

…Skipping a rate hike at a coming meeting would allow the committee to see more data before making decisions about the extent of additional policy firming.

And here’s Philadelphia Fed President Patrick Harker, also on Wednesday:

I think we can take a bit of a skip for a meeting and, frankly, if we’re going to go into a period where we need to do more tightening, we can do that every other meeting.

And just like that, the 60% bet on a rate-hike in June has swung the other direction, with 69% odds that the Fed will now leave rates unchanged.

As we noted in the Digest earlier this week, these Wall Street odds are so inconsistent that they’re more about entertainment than insight at this point. However, as my colleague Luis Hernandez astutely pointed out, they still provide a great snapshot of sentiment, which is very helpful as we try to get a bead on the markets.

But while a June “pause” is the leading narrative of the moment, the JOLTS report and this morning’s payrolls report might push the Fed members back into the “hike” camp

On Wednesday, we learned that job openings unexpectedly rose in April.

The Labor Department’s JOLTS data showed that after three straight months of declines, job openings jumped in April, reaching 10.1 million.

And this morning, the Labor Department’s payrolls report came in not just hot but scalding.

Whereas the Dow Jones estimate was for 190,000 new jobs in May, the actual number was 339,000.

Meanwhile, average hourly earnings, which the Fed watches very closely, rose 0.3% for the month. That was in line with expectations.

Now, the different responses to these data are interesting. And the report offers a great litmus test for whether you lean bull or bear.

For example, here’s CNBC with the “bull” take. Below is its headline following the JOLTS report:

A ‘pleasant’ surprise: Strong job numbers, low layoffs show no ‘major indicators’ of a recession, economists say

For the “bear” perspective, here’s The New York Times:

The jump in openings may put pressure on the Federal Reserve to take interest rates even higher.

The statistical relationship between high job vacancies, as calculated by the government, and low unemployment has been frequently cited by the Federal Reserve chair, Jerome H. Powell, as a key sign of the labor market’s being “unsustainably hot” and “clearly out of balance, with demand for workers substantially exceeding the supply of available workers.”

Regular Digest readers know that I personally lean bearish in this situation. I’m hardly a perma-bear; rather, I’ve just begrudgingly concluded that the Fed is hellbent on vanquishing inflation (after embarrassing itself via “transitory” inflation), and it’s willing to accept a recession as the collateral damage of that war.

Through this lens, a cheer for this flurry of shockingly strong labor market data seems odd to me because the Fed is likely to respond to the very same data with a groan.

Plus, regardless of whether the Fed pauses in June or not, it sounds increasingly likely that the Fed will hike rates at least one more time this year – especially given data like the JOLTS and payrolls reports.

Even the dovish Fed members, like Jefferson who we referenced above, are explicitly noting that a pause in June isn’t necessarily the end of rate-hikes.

Here’s Jefferson:

A decision to hold our policy rate constant at a coming meeting should not be interpreted to mean that we have reached the peak rate for this cycle.

Another Fed hike this year, and/or a Fed that simply holds rates at current, elevated levels, increases the chances of major economic fallout…even if we’re not close to a recession at the exact moment.

But even if we avoid a recession and enjoy a pillowy-soft landing, we need perspective about where the stock market is today

It might feel like 2022 brought a brutal bear market that decimated stocks, and now we’re finally seeing the first few steps of a fledgling bull market that’s rising out of gutter valuations.

That’s not the case.

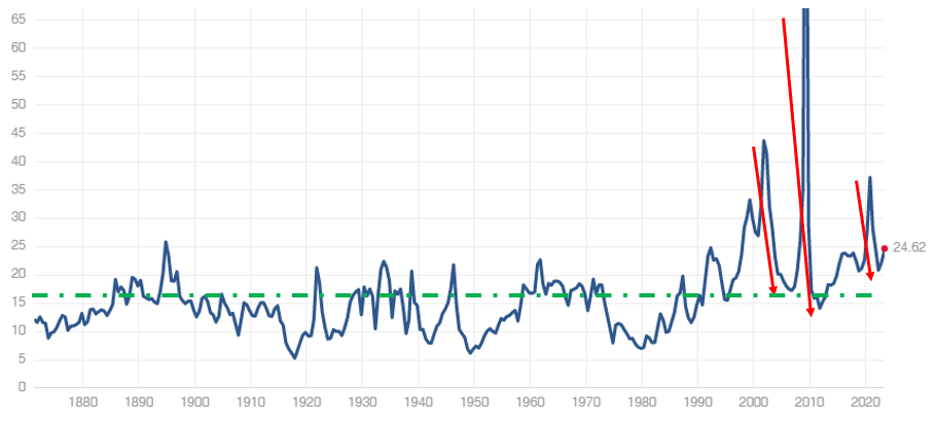

The S&P’s price-to-earnings (P/E) ratio clocks in at an expensive 24.62. The long-term average is 16.

A few years ago, the research shop Bespoke analyzed bull markets since 1942 and found that the average bull market begins with a starting PE ratio of 13.1 and ends with a final PE ratio of 18.9.

We’re nowhere close to a “beginning bull market” P/E ratio.

Frankly, we’re not even that close to a “ending bull market” P/E ratio. We’re almost 30% more expensive than where Bespoke said bull markets end, despite last year’s crash.

Now, a warranted pushback would be, “Okay, Jeff, then explain last year’s bear market. What was that?”

Well, perhaps, it was simply the bleed-off of an irrationally-expensive market value that returned us to just an “expensive” market value.

Take a look at the chart below for perspective, which shows the S&P’s P/E ratio all the way back to 1870

The dotted green line is the average P/E value (which we’re miles above).

I’ve also added red “down” arrows to show the “bleed-off,” as I just called it, from the three major P/E peaks over the entire stretch.

As you can see, those peaks are: 1) the high surrounding the Dot Com bubble, 2) the high surrounding the Great Financial Crisis, and 3) the high surrounding the post-Covid market bubble.

Source: Multpl.com

Source: Multpl.com

Note our current value, then follow that level all the way to your left on the chart…

Not very many readings up here, are there? We’re in pretty rare air.

Now, let’s be clear about what this does and does not mean…

The market could absolutely soar from here. That’s what happens when animal spirits strike. And with a growing sense of investor optimism, that could be happening right now.

But if it does, let’s analyze it correctly – it would be an expensive market becoming even more expensive. It would not be a bargain-valuation-baby-bull taking its first few steps.

This difference has major implications for how long the market might remain in bull mode, as well as how you decide to play it.

At some point, valuation will matter

As I just noted, investors are increasingly excited right now.

There’s the resolved debt ceiling issue… the prospect of the Fed pause… and, of course, artificial intelligence stocks.

Earlier this week in the Digest, we pointed out the absurd valuation of AI-poster-child Nvidia, which trades at roughly 40X revenues – not profits, but revenues.

Now, when you have that kind of price, there’s zero room for anything other than perfection.

Case in point, another AI darling, C3.ai.

Like Nvidia, C3.ai has seen astonishing gains this year as investors have stampeded into all things “AI.” As of Tuesday, the stock had exploded 293% in 2023.

Source: StockCharts.com

Source: StockCharts.com

For context, C3.ai isn’t profitable. So, we can only value it by its revenues, not earnings. And as of a few days ago, investors were willing to pay nearly 18X-revenues for the stock.

That’s not as high as Nvidia at 40X earnings, but it’s still absurdly expensive – especially for a company that’s operating at a loss. It’s a “priced for perfection” valuation.

Well, on Wednesday, C3.ai reported earnings. They weren’t bad. But they included the guidance that upcoming revenues will be less rosy than Wall Street wanted.

Let’s say it was an “imperfect” earnings report.

But what happens when “priced for perfection” runs into “imperfect”?

Well, you get a 27% crash in less than three trading sessions.

Source: StockCharts.com

Source: StockCharts.com

At some point, valuations will matter again – whether we’re talking about the high-flying AI stocks or the broad S&P

Be ready for that. But in the meantime, the market looks like it wants to climb.

So, what do we do?

Well, earlier this week in the Digest, we pointed out how adopting a “trading” mindset is a great way to handle today’s market, enabling you to remain in a bullish despite frothy valuations.

And with that mindset, where would you look for major gains today?

Well, we’ve already hit on it – AI. And our own Luke Lango is pounding the table on using AI to generate big money today:

The AI Boom is here, and folks, it is just getting started.

Call it a bubble. Call it overrated. But it’s neither. AI is the biggest technological paradigm shift since the internet. It is the real deal. It’s going to change the world.

And, unless you prepare for it, AI will kill your investment portfolio, too.

Why?

Because AI will permanently split society. You may think we live in a world of “haves” and “have-nots” today. But that divide is only going to get so much bigger in the Age of AI.

Today’s Digest is running long so we won’t delve into more of Luke’s research here. But I encourage you to click here for more.

Stepping back, as you make money from today’s climbing market, remember our broad context…

The Fed most likely isn’t done hiking rates… high rates are still squeezing parts of the economy and the U.S. consumer … and valuations aren’t anywhere in the arena of “discount” …

So, enjoy the bullishness, but have a plan for what you’ll do if/when it begins to fade.

Have a good evening,

Jeff Remsburg

More From InvestorPlace

- Buy This $5 Stock BEFORE This Apple Project Goes Live

- Wall Street Titan: Here’s My #1 Stock for 2023

- The $1 Investment You MUST Take Advantage of Right Now

The post So, Now Itâs a June Pause? appeared first on InvestorPlace.

Argentina Is One of the Most Regulated Countries in the World

In the coming days and weeks, we can expect further, far‐reaching reform proposals that will go through the Argentine congress.

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

A weird week of macro data – strong jobless claims but…

Fed Pivot: A Blend of Confidence and Folly

Fed Pivot: Charting a New Course in Economic Strategy Dec 22, 2023 Introduction In the dynamic world of economics, the Federal Reserve, the central bank…