Economics

What The #$%& Is A Shallow Recession

What The #$%& Is A Shallow Recession

This week, DataTrek founder Nick Colas is visiting his in-laws in Memphis for the Thanksgiving holiday,…

What The #$%& Is A Shallow Recession

This week, DataTrek founder Nick Colas is visiting his in-laws in Memphis for the Thanksgiving holiday, and as he notes, contact with what New York finance types call “the real world” is always an educational experience, given his usual cloistering in midtown Manhattan. To celebrate his brief freedom from the Big Apple, if only for a few days, are two brief thoughts based on a few interactions during his time here.

Below we excerpt from the latest Morning Briefing by Nick Colas of DataTrek

#1: What the #@$% is a shallow recession? My hotel’s breakfast area had business TV on this morning, and one of the hosts said, “markets are expecting a shallow recession next year”. She was not wrong. US equities trade for 18x current earnings, which strongly implies either no diminishment of corporate earnings or, at worse, a dip sometime in 2023 but then a swift recovery.

An older gentleman sitting opposite me at group table shook his head and grumbled the question noted above. His observation, implying that any recession can be “shallow” is at best euphemistic and at worst delusional, is also not wrong.

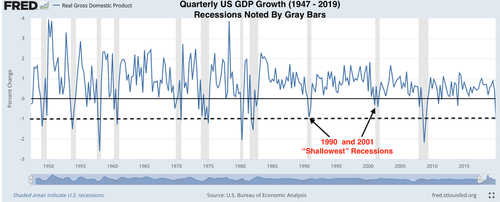

Since World War II, the shallowest recessions in terms of their effect on US GDP growth were in 1990 and 2001. The chart below shows quarterly real GDP growth from 1947 to 2019, with the 11 official NBER recessions over that period noted by the gray bars. We have put a dotted line across the 1 percent contraction level. All but the 1990/2001 recession exceeded that number.

Many readers will recall the 1990 and 2001 recessions, and I am fairly sure none would think of them as “shallow”. The first was due to an oil shock caused by Iraq’s invasion of Kuwait. US unemployment went from 5 to 8 percent over 2 years. The second was caused by the bursting of the dot com stock bubble and the 9-11 terror attacks. Unemployment rose from 4 to 6 percent.

The lesson here is that even “shallow” recessions have real world outcomes and, in the case of 1990 and 2001, came with other problems. Yes, perhaps the Fed can thread the needle of reducing inflation without causing a steep recession. We certainly hope it can. But I think it will pay to have some of the skepticism offered by my dining companion until that result becomes somewhat clearer.

* * *

#2: Help wanted. There are still many small businesses in the Memphis area looking for workers, especially those with seasonal labor needs heading into the holidays. The shortage of workers is evident here, as it is across the country. It has been thus for over 2 years, with wage inflation a necessary byproduct of that phenomenon.

The chart below shows US labor force participation (people in the workforce divided by the total population) for 25 – 54-year-olds (in red, left axis) and all adults (black line, right axis) from 2015 to the present.

Two points on this data:

- Prior to the pandemic, aggregate and 25 – 54 LFP was rising. The former hit 63.4 percent in February 2020, its highest level since June 2013. The latter got up to 83.1 percent, the best level since May 2013. A strong, late cycle US economy was pulling Americans into the workforce.

- Today, both LFP levels remain below their pre-pandemic highs. Working-age (25 – 54-year-olds) LFP is 0.4 points lower, which translates into 520,000 “missing” prime-aged workers. Total LFP is down 1.2 percentage points, or 3.2 million people.

The upshot here is that, despite population growth, there are scarcely more workers in the US now than at the start of the Pandemic Crisis. According to BLS data, the civilian non-institutional American population has grown by 1.9 percent since February 2020. The total number of Americans in the workforce has only grown by 0.5 percent.

Linking this discussion to the prior point about recessions, it is worth noting that every economic downturn since the 1980s has seen labor force participation either stay flat or decline. In the 1970s/early 1980s, LFP was stable through recessionary periods primarily because women were still entering the American workforce. In the 1990, 2001, and 2007 – 2009 recession, LFP fell by 2 points or more during/after each downturn.

The lesson here is that a recession does not draw people into the workforce, so the current labor shortage is unlikely to ease very much in a “shallow” recession. An economic downturn should, however, reduce wage inflation to some degree if employees feel they no longer have bargaining power with respect to their pay. Still, this may not be enough to bring wage growth in line with productivity growth if the supply of labor contracts over the next 1-2 years.

Tyler Durden

Sun, 11/27/2022 – 21:30

inflation

markets

fed

bubble

Argentina Is One of the Most Regulated Countries in the World

In the coming days and weeks, we can expect further, far‐reaching reform proposals that will go through the Argentine congress.

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

Crypto, Crude, & Crap Stocks Rally As Yield Curve Steepens, Rate-Cut Hopes Soar

A weird week of macro data – strong jobless claims but…

Fed Pivot: A Blend of Confidence and Folly

Fed Pivot: Charting a New Course in Economic Strategy Dec 22, 2023 Introduction In the dynamic world of economics, the Federal Reserve, the central bank…