Energy & Critical Metals

Embrace the case for India? ‘It just makes too much sense’ as wealth shifts from West to East

India has the need, the capability and the determination to shift very quickly into another tier of economic superpower, particularly … Read More

The…

India’s having so many moments right now, it’s difficult to keep up.

Luckily, the Indian Prime Minister Narendra Modi tweets like a champion.

Today’s talks with PM @AlboMP were comprehensive and wide-ranging. This is our sixth meeting in the last one year, indicative of the warmth in the India-Australia friendship. In cricketing terminology- we are firmly in T-20 mode! pic.twitter.com/uD2hOoDL6H

— Narendra Modi (@narendramodi) May 24, 2023

The Times of India enjoyed the Guard of Honour for the Indian PM at Admiralty House in Sydney on the final day of his rockstar visit – his first trip here since 2014.

Then, getting down to brass tacks, Modi and our Albo signed off an some official agreements, including one on mobility that will lubricate the movement of professionals and education exports between here and there.

They also came to terms on a bilateral Green Hydrogen Task Force to promote cooperation on punching out as much of the gas as possible as part of their joint efforts to get transitioning.

Modi called the migration deal as “strengthening the living bridge” between India and Australia, which was pretty classy, since about 3% of us are of Indian heritage. Albo was in India to watch our crap cricket team just two months ago.

The world’s leading producer of milk? Neither New Zealand nor A2M. India quietly churns out almost a full quarter of global milk production – then in order of descent the Americans, Chinese, Pakistan and Brazil.

This week, the commodity data firm Mintec says the price of milk in India is rising fast. Up about 15% and that’ll not stop until near Christmas.

Speaking to India’s Economic Times, RS Sodhi, ex MD at India’s largest dairy producer, Gujarat Cooperative Milk Marketing Foundation, put the the “extraordinary increase in milk and dairy products”, down to higher feed costs, cattle disease and… an increase in demand for ice cream.

“In the last 15 months there has been [an] extraordinary increase in milk and dairy products, around 14-15%,” said RS Sodhi, former managing director of India’s number one dairy company, Gujarat Cooperative Milk Marketing Foundation.

Foxconn which makes things for Apple (APPL) has just broken ground on what will be a giant half a billion US dollar mega-factory in Telangana state, not even a month after Modi received a visit from none other than Apple CEO Tim Cook.

Foxconn has been with Apple for the years of an old donkey and is said to directly produce almost 75% of the world’s iPhones.

The new Telangana factory will employ 25,000 workers “in the first phase,” according to a tweet from the government of Telangana.

The India opportunity will increasingly be better captured by foreign investors who are allocating directly to India, rather than in a Global or Emerging Market Fund, India Avenue’s Mugunthan Siva told Stockhead, “given the need to identify the next categories to drive India‘s growth i.e. manufacturing, rural, technology etc, whilst consumption and financial services remain important.”

Modi and Albo said in a joint statement from The PM’s office that the visit “reinforced their commitment to an open, prosperous and secure” Indo-Pacific region.

Bad luck China, especially since the PMs look determined to complete a free trade deal before the end of the year.

Foreign flows to India are made up of FDI (foreign direct investment) and FII (foreign institutional investors).

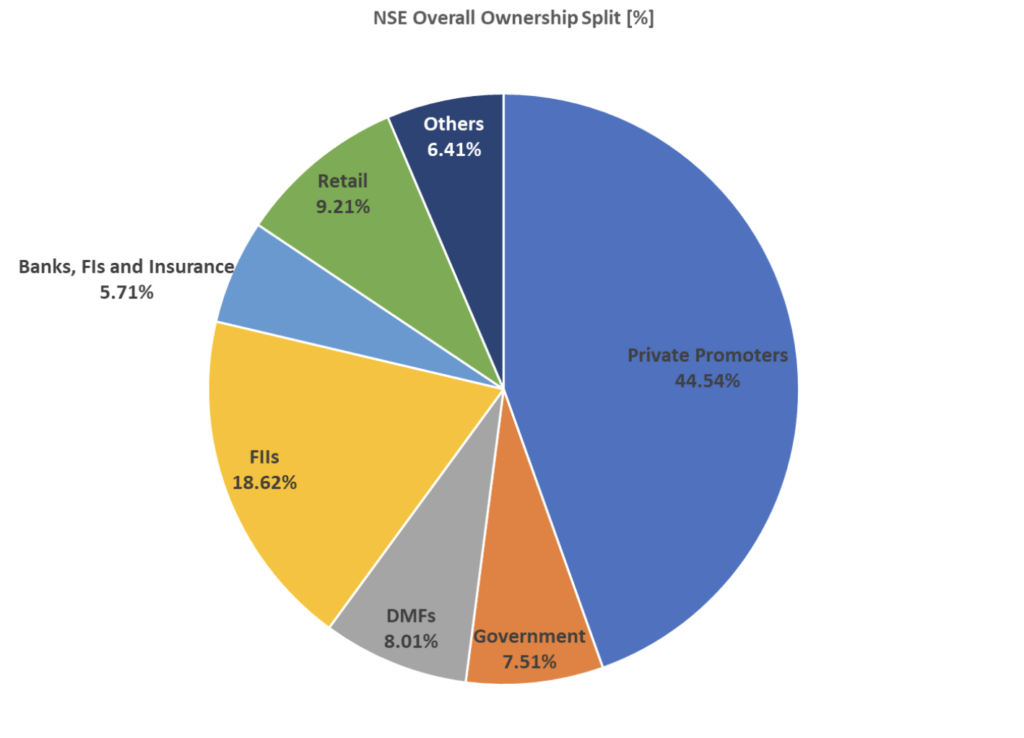

FIIs typically have driven market direction given that local promoters/founders who own around 45% of market cap tend to be non-sellers. Therefore, according to India Avenue, FII flows have a high correlation to Indian equity market movements.

And the markets are moving.

Our own James FREE Whelan wrote a fortnight back that his team initiated the long on the Global X India ETF.

“I’m starting to bang the drum on the trade into India. There’s a lot to love about what’s happening in India. In the digital and renewable space one should allow the juices of excitement to percolate,” he told us.

“The more I look at it the more I see it as being something that should have been in portfolios long ago and should stay for a long time to come.

“Eastspring Investments put out a lengthy report off the back of a survey they do of local business leaders. The key takeaway reinforces what I’ve been saying with regards the transfer from China to India as the market with the most upside.

“I’ll put the easy part in front of you…

And here’s the link to the report. It’s very good.

Stats I have loved

Whelan said he’s fascinated by the depth of India’s tech talent.

“A few years back the tech pool there at 3.8 million, was behind both China and the US. With a growing, younger population and a strong digital education focus, you’d reckon that’d be changing fast.”

India has the need, the capability and the determination to shift very quickly into another tier of economic superpower, particularly in digital and renewables, Whelan told Stockhead earlier this month.

According to the Financial Times, the southern state of Karanataka has been growing at 8% p.a. for the last decade and doubling average incomes through the last decade to US$3800.

“That growth adds to money in wallets (digital or otherwise) which adds to the growth in Systematic Investment Plans regular savings plans investing in Indian managed Funds (like our superannuation system but optional) and that then adds to continued equity growth in Indian stocks,” James said.

“It just makes too much sense.”

DIIs DIY

Mugunthan says foreign investors have tended to lean into buying financials (Banks, Life Insurance, NBFCs) and consumption companies as a way to play the local demand story in India.

“However, the problem is these stocks are quite expensive and given the appearance of making India‘s equity market as a whole look expensive as most of its large and mega cap companies are in fact Banks and Consumption companies.”

It’s important to understand just how quickly local investors (referred to as DIIs) are now pulling up level with FIIs in terms of ownership of market cap, he says, and as a result have a far greater impact on the overall behaviour of the market.

“These investors have a different opportunity set and as such are not just looking for “India plays” but rather trying to find the best opportunities in India and are more valuation conscious given the broader India opportunity set (FIIs tend to invest mainly in the large and liquid mega and large caps, due to their size).

“Thus we note the changing pattern of India‘s market towards a more value oriented market. Local investors will continue to increase as increasing “financialisation” takes place (shift towards financial assets) which leads to increasing equity ownership.”

This is part of the shift of the world’s wealth base over time from the West to the East, given demographics and employable population.

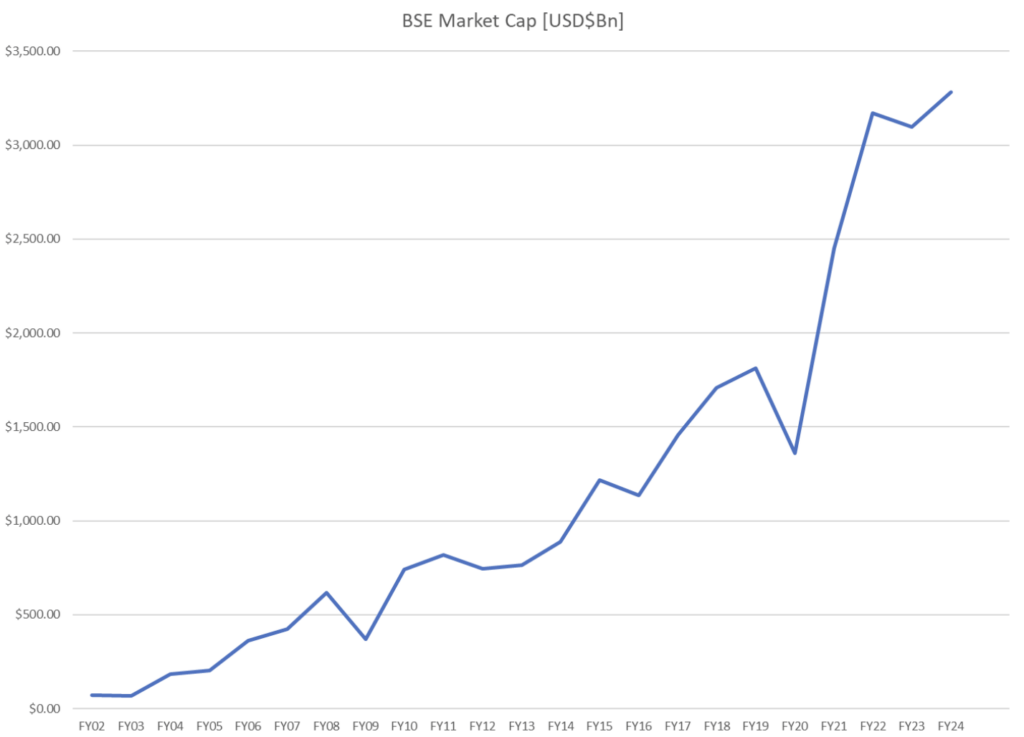

India Avenue analyst Ramanesh Mahendran sent Stockhead a bunch of data picking apart the shape and make up of India’s stock market (BSE/NSE) over the last 20 years, where there’s been a hitherto comparatively quiet boom.

From meagre beginnings this month the market’s current combined value is US$3.5 trillion.

The graph below clearly shows the pace of growth, Ramanesh adds, referring to the near vertical post-COVID spike.

“The next graph also highlights that a considerable portion, approximately 45%, of the stocks are owned by either promoters or founding families. While this isn’t shocking, it’s interesting to consider as a factor affecting India’s future stock market growth.

Furthermore, he says, it’s no flash in the pan.

“A lot of these companies are incredibly reluctant to sell their family shares in a fear of losing the majority stake.”

So what does the composition and structure of ownership in the Indian stock market actually mean to us?

“Looking at the graph above for the month of December in 2022, Foreign Investors accounted for 18.62% of the total ownership in the stock market,” Ramanesh says.

“This has decreased from upwards of 22% since the beginning of the COVID-19 period. This can be explained by the global economic slowdown which led to the general outlook of investing declining on the global stage.”

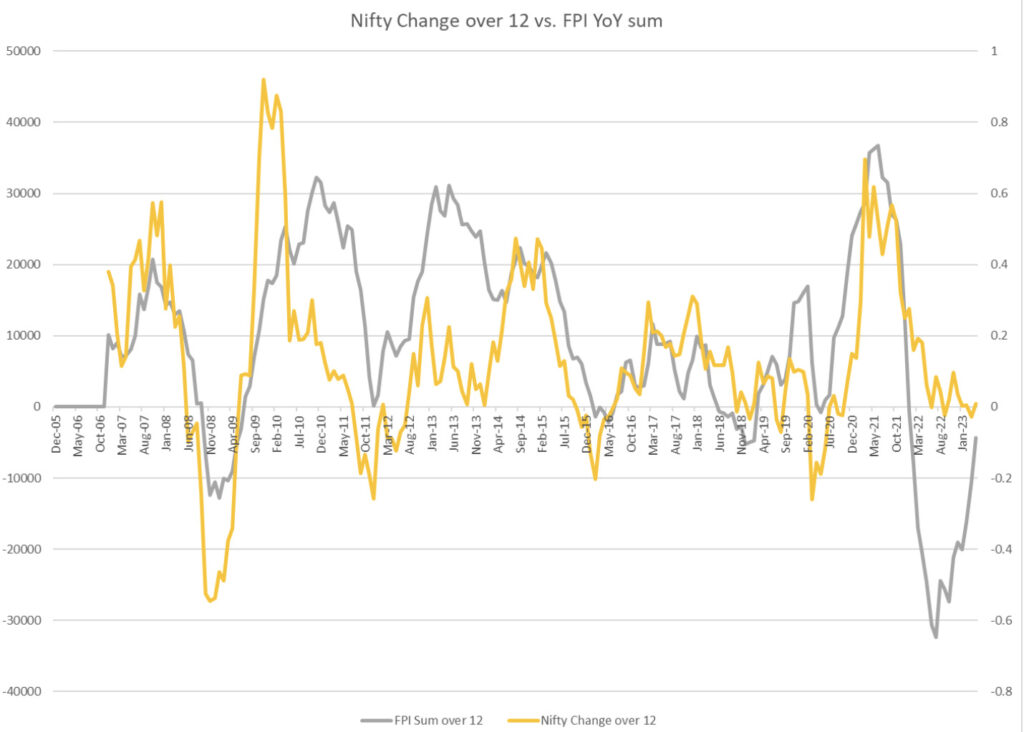

Ramanesh says this next one (below) outlines the percentage change of India’s Nifty 100 over 12 months against the sum of FPI over a 12-month period.

“While the message illustrated may not be completely correlated, it paints the image that foreign investment follows the clear pattern established by the Nifty 50.”

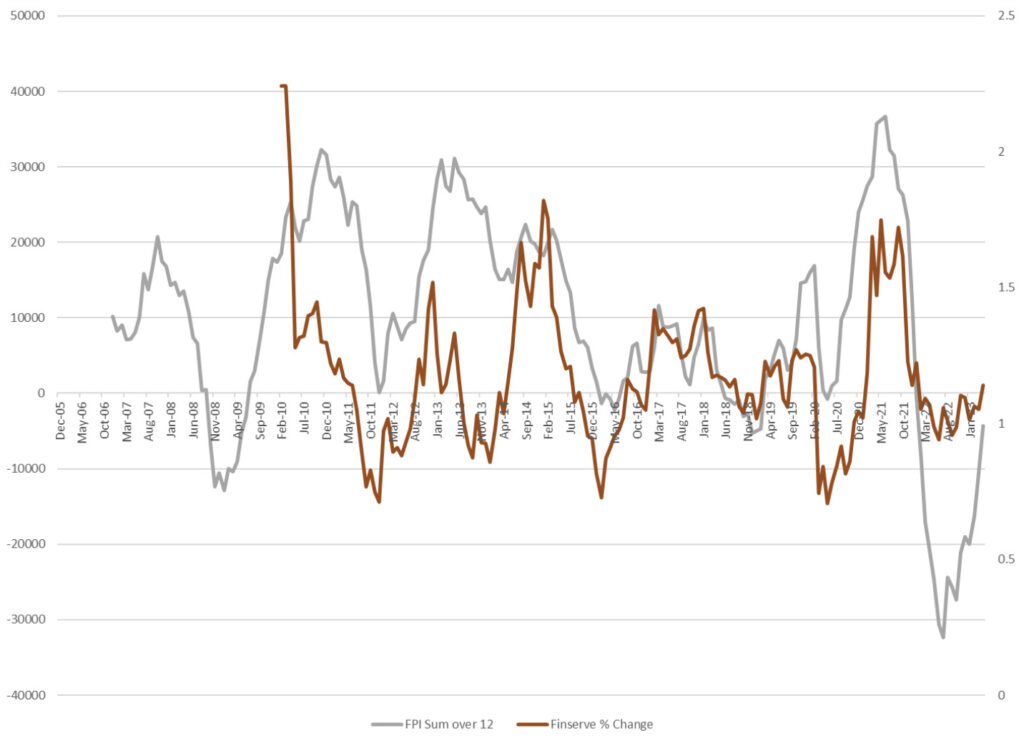

And here we have another spiky fella which India Avenue believes “clearly plots the FPI sum over the past 12 months against the change in Nifty Financial Services” over the same time.

While this one is similar to the previous data set, Ramenash says in his eyes “it is a lot more correlated.”

“The peaks and troughs are both implying and justifying the idea that the Financial Service Sector receives more attention from foreign investors.”

At last: Home grown momentum

Local Indian investors – individuals, mutual funds and retail investors – have all become far more dominant players over the last decade according to Mugunthan.

“At the end of last year – not a great one for most of the major global markets – here in India retail investors actually accounted for 91.1% of all mutual fund accounts active in India.”

And yet, according to surveys by the RBI, less than 3% of Indian households are actively investing in the stock market.

Now compared to more developed economies, the growth potential is off the charts, Mugunthan says. “Which is why we don’t even have one – here the number is around 36% of adult owning ASX stocks, while in America the number is thought to be up around 58%.”

“As India’s general investing culture begins to shift towards equities as the economy develops, this number is expected to grow to a very significant level.”

Breaking free of the moorings

“One of the advantages of this trend towards equity investing locally is that it offsets the effects that foreign investing holds upon the market. Due to a large portion of the stock market being held by families and promoters, volatility can typically be set by foreign investors aiming for a more short-term investing ideology,” Ramanesh continues.

“With investing becoming more of a trend among households, it’s easy to understand why it will reduce the overall volatility of the stock market itself.”

There’s other exciting quirks that Aussies and other – let’s face it, wildly ignorant – prospective foreign investors have absolute NFI about.

Indian investors have also been noted to follow and hold a greater focus upon relative valuation locally rather than globally, Ramanesh tells me.

“What this means is that Indian investors are more interested in the cheaper stocks that are available to them, due to their disposable income at a household level not being very high.”

In comparison, apparently the foreign and more sophisticated investors tend to place a much greater emphasis on capitalising on India’s growth story, chasing the big narratives and investing in certain industries which they reckon will benefit in the coming years such as consumer goods or banks.

“The focus upon the relative valuation locally allows for greater potential returns,” Mugunthan says. A little excitedly.

“With local investors entering and finding these cheaper stocks, the market will become more investor balanced, and there will be a greater balance between small, mid and large cap investors.”

The view from Europe

Vincent Mortier Group chief investment officer at the French asset management giant Amundi is another with an upbeat assessment.

Mortier says while there’s risks to be aware of – most particularly across an often wild domestic political landscape and the uncertain evolution of commodity prices – India’s recent economic chops has all but elevated its status to ‘global growth engine’.

He also believes the fast-moving geopolitical developments and India’s ability to retain a fairly agnostic position means its influence in the geopolitical arena is likely to strengthen.

“It has maintained relationships with various powers and is benefitting from the Western resolve to disentangle itself from China.”

India’s macro fundamentals are well positioned for a multi-year improvement in economic output and earnings, he says.

“Beyond the long-standing strength of its demographics, urbanisation and rising middle class, new factors are emerging that will accelerate investment opportunities in the country.”

Looking at equities, Amundi believes India’s long-term growth story is “appealing beyond its short-term valuation excess” and is getting good back up by better bank balance sheets, better corporate balance sheets, leaner cost structures, decent policy reforms and Production-Linked Incentives (PLI).

These factors also support the possibility that rupee could by due for a period of strength.

“The Indian rupee now appears more stable and can benefit in an environment of USD weakness. Despite the uncertainty, 2023 may be a better year for the rupee than 2022.”

What does all this mean for India?

This is all Mugunthan via email:

“Following foreign perceptions of investing returning to normal after the COVID-19 period, it is expected that foreign investors will likely return to India in the near-term due to the main advantages that the Indian economy itself presents.

The formalisation of the Indian economy will most likely act as a dominant factor as the economy continues to develop and GDP continues its growth path.

With the attention of domestic investors turned towards the small and mid-cap stocks, foreign investors will most likely continue to invest in the large and liquid stocks, which represent the foreign interpretation of the India stories, specifically in sectors such as Banking, Technology and Consumption.

Furthermore, this influx of domestic investors who seek to increase their savings will lead to a trend of value investing, allowing value investing to become more dominant in the upcoming timeline.

And finally, this will allow both foreign and domestic investors alike to focus upon and watch the emergence of industries like Real Estate, Pharma, Specialty Chemicals and Manufacturing.

These industries will undoubtedly have a strong and secure future in India and it is just a matter of time until investors realise this.”

The post Embrace the case for India? ‘It just makes too much sense’ as wealth shifts from West to East appeared first on Stockhead.

Uranium Exploration Company Announces Additional Staking in the Athabasca Basin

Source: Streetwise Reports 12/22/2023

Skyharbour Resources Ltd. announced an update from its Canada-based Falcon Project along with additional…

Tesla Launches New Mega Factory Project In Shanghai, Designed To Manufacture 10,000 Megapacks Per Year

Tesla Launches New Mega Factory Project In Shanghai, Designed To Manufacture 10,000 Megapacks Per Year

Tesla has launched a new mega factory…

Giving thanks and taking stock after “a remarkable year”

An end-of-year thank you to our readers, industry colleagues and advertisers before Electric Autonomy breaks from publishing until Jan. 2

The post Giving…