Mexico could run out of silver by 2026, worsening supply deficit – Richard Mills

2024.01.13

The world’s largest silver producer could mine all of its existing reserves within two years, throwing silver’s global supply-demand balance even further out of whack than it is currently.

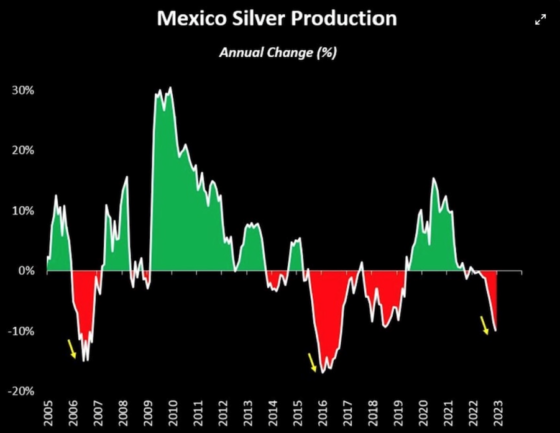

Mexico has regularly outputted 5,600 tons of white metal over the past 10 years, but has seen its reserves dwindle to just 37,000 tons. If mining continues at the current pace, Mexico’s silver reserves will be exhausted by the end of 2026, it was recently reported.

Silver production there is now declining double digits annually for the first time in almost a decade. This year, output is expected to fall by 16 million ounces because of the suspension of operations at Newmont’s Penasquito mine due to a strike. (The Silver Institute)

The country made headlines in 2022 when the government of President Andrés Manuel López Obrado nationalized the lithium industry.

According to Mining.com, The bill elevates lithium to the category of “strategic mineral”, declaring the exploration, exploitation, and use of lithium to be the exclusive right of the state. It also includes a clause allowing the state to take charge of “other minerals declared strategic” by Mexico…

Could silver be the next metal to be nationalized?

Since taking power in 2018, López Obrador has fought to reverse resource reforms under previous governments, which opened up the oil and electricity sectors to private investment. He has pushed a resource exploitation model that gives priority to state-controlled companies.

Last year, the Mexican government passed an overhaul of mining laws, including shorter concessions and tighter rules for permits. The reforms also reduced the length of mining concessions from 50 to 30 years. The earlier proposal was for 15 years.

Dan Dickson, the CEO of Endeavour Silver, a Canadian firm with two producing silver mines in Mexico, said the changes to concession terms would affect juniors’ ability to secure finance.

“We deplete our resources and need to make new discoveries to replace that supply. It will limit companies coming behind the operators to bring that additional supply on,” Dickson told the Financial Times.

The mining code changes also threaten to trigger a wave of litigation in Canada, where 70% of foreign mining companies operating in Mexico are based. Industry group Camimex has warned the legal reforms could jeopardize $9 billion of investment in the next two years.

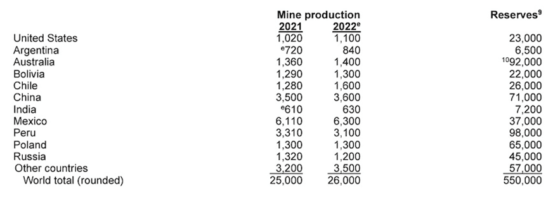

According to the US Geological Survey, Mexico produced 6,300 tonnes of silver in 2022, against world number two China’s 3,600 tonnes, and third-place Peru’s 3,100t.

While Mexican production has nose-dived in the past, it’s never been in conjunction with China demand this large, Silver Academy notes:

Chinese demand is so intense because of the global bifurcation of trade; they are now buying raw ore, as well as concentrate directly from silver producing countries.(the same thing is happening to China’s copper — Rick)

This is in no small part because their own production is also drying up.

The website points out that Latin America is favoring labor and environmental activism, and recent trends in Peru, Chile and Panama that have shut down mines, including First Quantum Minerals’ massive Cobre Panama copper-gold-silver operation.

Silver is often mined as a by-product of gold, copper and lead-zinc. A lot of silver is going to be taken offline by the closing of copper mines in particular. According to First Quantum, Cobre Panama produced 2.813 million ounces of silver in 2022, and 891,967 oz in the third quarter of 2023 before the Panamanian government forced its closure.

Other factors working against silver production are a low incentive price and higher input costs.

Most all-in-sustaining-cost (AISC) models do not account for the enormous sunken costs, in exploration and project advancement, before shovels even break ground. Silver’s cost of production is now over $24 per ounce, says Silver Academy, and at an adjusted minimum of $25.75/oz, miners are losing money. AISCs are expected to keep increasing due to rising labor and diesel costs.

2023 deficit

All of the above factors — falling production in Mexico and China, the top two producers; resource nationalism in Peru, the number 3 producer; too low of an incentive price; and higher input costs — are all feeding into a global silver supply deficit.

According to the 2023 World Silver Survey, the global silver market was undersupplied by 237.7 million ounces in 2022, which the Institute says is “possibly the most significant deficit on record.”

It took just two years of undersupply — the 2022 deficit and the 51.1 million oz shortfall from 2021 — to wipe out the cumulative surpluses from the previous decade.

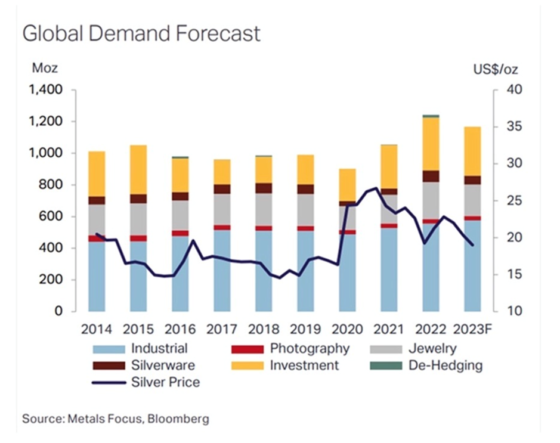

Global silver mine production is projected to fall 2% this year to about 820 million ounces, compared to forecasted demand of 1.2 billion ounces. First Majestic Silver’s CEO Keith Neumeyer recently commented that the solar panel and electric car industries now consume about 30% of mined silver supply. Moreover, he said one primary silver mine produces about 10 million ounces a year, meaning it has “zero impact” on the deficit, which represents many mines worth of production.

The Silver Institute forecasts a 140Moz silver deficit this year, the third consecutive annual shortfall, against robust silver industrial demand, which is expected to grow 8% to a record 632Moz. Key drivers include investment in photovoltaics, power grid and 5G networks, growth in consumer electronics, and rising vehicle output.

“We are moving into a different paradigm for the market, one of ongoing deficits,” said Philip Newman at Metals Focus, the research firm that prepared the Silver Institute’s data.

Metals Focus believes the deficit will persist in the silver market for the foreseeable future.

Industrial demand drivers

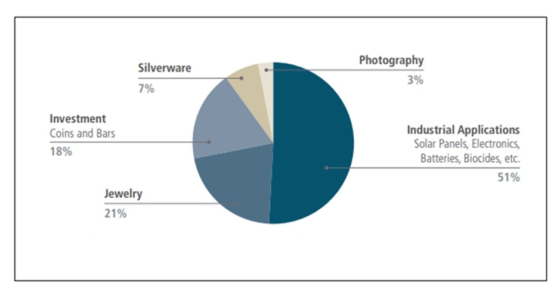

Much of silver’s value is derived from its industrial demand. It’s estimated around 60% of silver is utilized in industrial applications, leaving only 40% for investing.

Lately, silver has garnered a lot of attention of its “green” uses such as in solar and electric vehicles. Silver Academy states that silver is the critical mineral for net-zero economies, pointing out uses in hydrogen fuel cell cars, trucks, vans, ships, barges, ferries, satellites, robotics, AI, solar, wind power, in addition to over 10,000 other applications.

Solar

As the metal with the highest electrical and thermal conductivity, silver is ideally suited to solar panels. A 2020 Saxo Bank report stated that “potential substitute metals cannot match silver in terms of energy output per solar panel.”

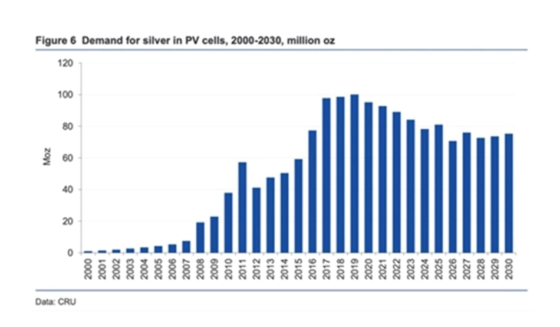

Using silver as conductive ink, photovoltaic cells transform sunlight into electricity. Silver paste within the solar cells ensures the electrons move into storage or towards consumption, depending on the need. It is estimated that approximately 100 million ounces of silver are consumed per year for this purpose alone.

Consider: For every gigawatt of solar, 500,000 ounces of silver are used. Just one manufacturing facility in Houston, built by Waaree Energies, India’s largest solar PV module manufacturer, will use 1.5Moz per year. Another plant on the same street will use 1Moz annually.

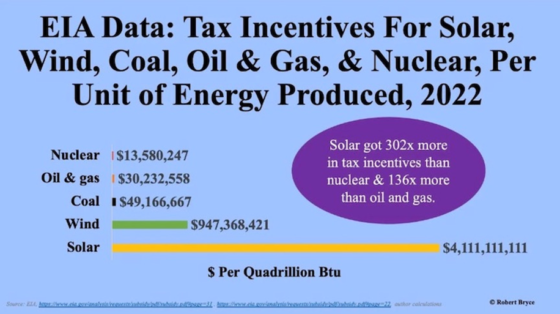

The solar industry is well-supported by the US government, and governments worldwide. The graphic below shows solar received 302 times more in tax incentives compared to nuclear, and 136X more than oil and gas.

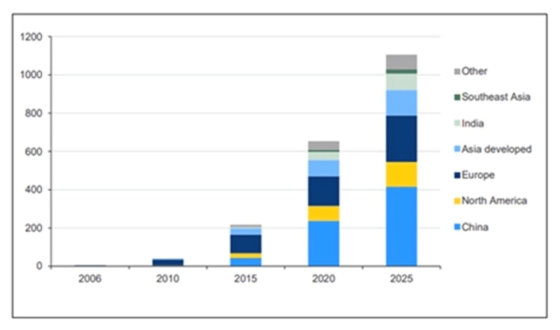

More and more silver is being demanded for use in solar photovoltaic (PV) cells, as countries adopt renewable energy sources.

This figure is expected to rise in the coming years, with continued growth of electricity demand and renewable energy aspirations all pointing to rising solar power penetration.

Source: The Silver Institute & CRU Consulting

One projection has annual silver consumption by the solar industry growing 85% to about 185 million ounces within a decade, according to a report by BMO Capital Markets. Solar Power Europe expects global solar power installations will more than double in three years to reach 2.3 terawatts by 2025, up from 1 terawatt in 2022.

The US solar industry will likely be one of the leading drivers of silver demand. Installations grew 43% year over year in 2020, reaching a record 19.2 gigawatts of new capacity. By 2030, solar installations are expected to quadruple from current levels, according to a report from the Solar Energy Industries Association and Wood Mackenzie.

While each solar panel only uses a small amount of silver, with the demand for solar growing every year, it adds up. A new Australian study projects solar panels could use most of the world’s silver reserves (550,000 tonnes according to the US Geological Survey) by 2050.

A research paper by the University of New South Wales found solar manufacturers would likely require over 20% of the current supply by 2027, and between 85 and 98% of it by 2050.

The paper also noted that more efficient ‘N-type” technologies being developed, require more silver than current ‘PERC’ cells that make up over 80% of the market.

Another boost to silver demand may come from the “One Sun, One World, On-Grid” initiative, launched in the fall of 2021 by Australia, France, India, the US and the UK. The initiative plans to connect solar energy grids across borders.

Copper and silver: the electrical metals

5G

5G technology is set to become another big new driver of silver demand. Among the 5G components requiring silver, are semiconductor chips, cabling, microelectromechanical systems (MEMS), and Internet of things (IoT)-enabled devices.

The Silver Institute expects silver demanded by 5G to more than double, from its current ~7.5 million ounces, to around 16Moz by 2025 and as much as 23Moz by 2030, which would represent a 206% increase from current levels.

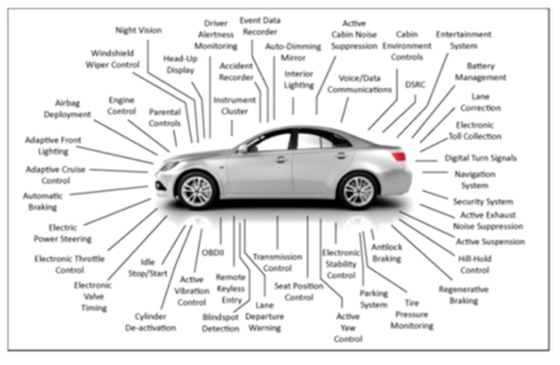

Automotive

A third major industrial demand driver for silver is the automotive industry. Silver is also found in many car components throughout vehicles’ electronic systems, and despite not being used in batteries, its superior electrical properties make it hard to replace across a wide and growing range of automotive applications.

A Silver Institute report says battery electric vehicles contain up to twice as much silver as ICE-powered vehicles, with autonomous vehicles requiring even more due to their complexity. Charging points and charging stations are also expected to demand a lot more silver.

Statista reports there were 2.7 million public charging points worldwide at the end of 2022, with South Korea “leading the charge” at 563 charging stations for EV — by far the highest density of the world’s largest electric-vehicle markets.

SI estimates the sector’s demand for silver will rise to 88Moz in five years as the transition from traditional cars and trucks to EVs accelerates. Others estimate that by 2040, electric vehicles could demand nearly half of annual silver supply.

Source: The Silver Institute

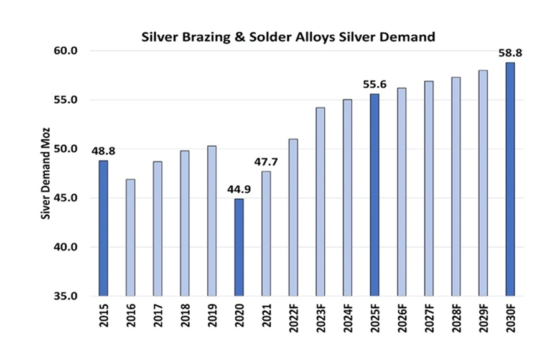

Brazing & soldering

In 2021, brazing and soldering alloys used 47.7Moz of silver, representing 9.3% of the total industrial demand for silver that year. Last year brazing and alloys accounted for 49Moz.

By 2030, the demand for silver used in brazing and soldering is forecast to reach 58.8Moz, a 23% increase over 2021, according to a Silver Institute report titled ‘Silver in Brazing and Solder Alloy Materials’.

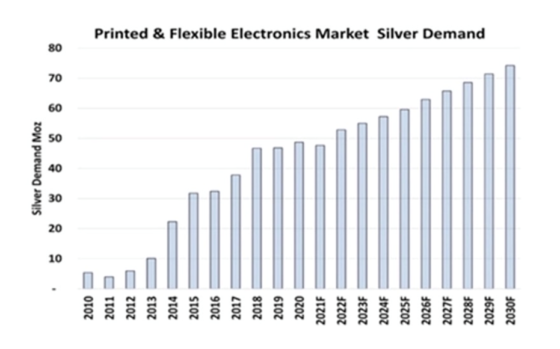

Electronics

Finally, silver demand for “printed and flexible electronics” is forecast to increase 54% over the next nine years, rising from 48Moz in 2021 to 74Moz in 2030, meaning a consumption of 615Moz during this time frame.

A Silver Institute news release describes them as “mainstays” in a variety of electronic products, including sensors that measure everything from temperature, pressure and motion, to moisture, relative humidity and carbon monoxide. They are also used in medical devices, mobile phones, appliance displays and consumer electronics.

In 2021, a comprehensive report by Sprott titled ‘Silver’s Clean Energy Future’ found that three areas of growing demand for silver — solar, automotive and 5G — potentially account for more than 125 million ounces in 10 years. This doesn’t include the growth in investment demand for silver, which as mentioned represents about 40% of usage.

Source: Precious Metals Commodity Management LLC

Above-ground silver

Silver is interesting in that there is the same amount of investable silver above ground as there is gold, because 60% of silver goes into industrial uses and 80% of that end up in landfills. Just 40% is used for investing.

Looking at mined silver versus gold, if we take the 60% of silver used for industrial purposes and subtract the 80% that gets thrown into landfills, silver should be more valuable yet the current silver to gold price ratio is 88:1.

Monetary demand

Silver, like gold, is a precious metal that offers investors protection during times of economic and political uncertainty.

After Russia’s invasion of Ukraine, the flight to safety subsequently sent silver prices past the $26/oz mark, which was last seen in August, 2021.

This silver rally proved to be a flash in the pan, however. An aggressive interest rate hike campaign by the US Federal Reserve, along with a high US dollar, has kept the safe-haven metal in check.

Still, there are reasons to believe that longer term, silver will rebound. One is the same reason to be bullish on gold, i.e., that continued monetary debasement due to high inflation, out-of-control spending and monstrous government debt, will eventually push bond and stock investors over to precious metals.

Assuming the US Federal Reserve proceeds to cut interest rates, likely around the mid-point of the year, silver and gold could both rally, as the opportunity cost of holding metals gets lower.

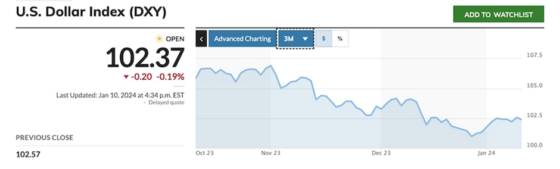

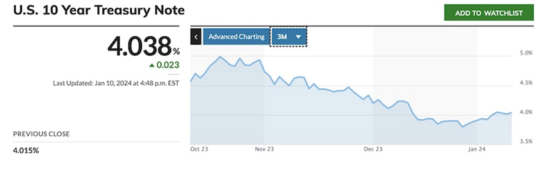

Gold and silver typically trade in the opposition direction of the US dollar, an alternative safe-haven asset. While the dollar’s value, measured by the US dollar index (DXY), has climbed in tandem with the Fed’s interest-rate-hiking cycle, lately it has begun to weaken, as interest rates such as the 10-year Treasury yield fall, and the market comes to believe that monetary easing is around the corner.

DXY is currently sitting at 102.37, compared to 106.12 on Nov. 2, a decline of 3.6%.

At the beginning of November, a statement by one of the Federal Reserve’s more hawkish voting members caused gold to spike and the dollar to slump. Christopher Wallen suggested the Fed could start lowering rates if inflation continues to decline “for several months,” adding that “There is no reason to say we will keep it really high.”

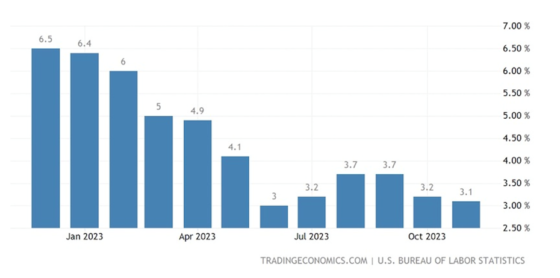

Inflation has already halved from 6.5% in December 2022, to 3.1% in November 2023, a five-month low. It peaked at 9.1% in June 2022.

One of the things gold (and silver) investors are watching for is a flip from positive real interest rates to negative real rates. The latter is typically associated with gold bull markets.

Things are certainly moving in the direction of monetary basement. Economist Daniel Lacalle says “the massive destruction of the purchasing power of the currency continues,” with “gold now the only real defense against the loss of the purchasing power of fiat currencies.”

Gold is the solution to current debasement

Considering that central banks are looking to impose their own digital currencies, gold proves again that it is an essential asset in a portfolio where investors try to escape the collapse of money as we know it. According to Lacalle,

“The problem in 2024 is that soft landings are rare, that monetary contraction and rate hikes will show their true impact with the typical lag of twelve to fourteen months since the last hike, and that the federal government’s fiscal policy will continue to drive deficits and debt higher, which means consuming more newly created units of currency and debasing our salaries and savings. If the threat of central bank digital currencies is confirmed, gold will prove again its quality as a reserve of value and means of payment, but it is also likely to show that it is one of the few assets that protects investors in a recession.”

Fiat currencies are being destroyed because of reckless money-printing by governments. That’s a lesson not learned that reverberates throughout monetary history; when government, any government, comes under financial pressure they cannot resist printing money and debasing their currency to pay for debts.

Ascent of central bank digital currencies bodes well for gold

You don’t purchase PMs to take advantage of short-term price fluctuations in the market, you buy them because they will always gain in value compared to paper money.

Over time, gold is a store of value because it is not subject to the inflationary pressures fiat currencies are. We can only guess what the Federal Reserve is going to do next. What we do know is that all currencies are weak, they’re not “real money”, and that our portfolio has to have a high proportion of physical gold and silver.

Buy signal

Gold and silver tend to trade in tandem. When gold pushes higher, silver usually lags, but then it can outperform gold.

When precious metals rallied in 2020, on the back of lockdowns, interest rates slashed to zero, QE, and general market fear, silver’s gain was double that of gold. The price ran up 43% from January to December, 2020, compared to gold’s ‘mere’ 20.8% rise. Earlier in the year, as gold punched above $2,000 an ounce, a 39% gain, silver rallied to nearly $30 an ounce, a 147% increase.

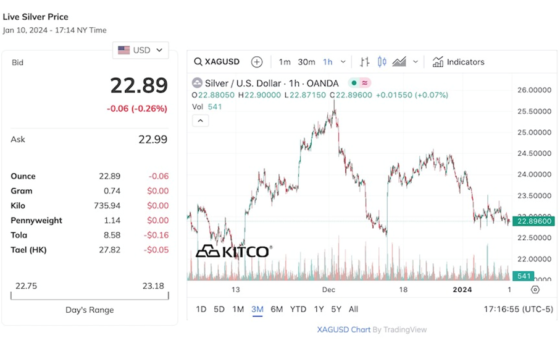

At $22.89 an ounce, silver is significantly under-valued. In December, when gold hit a record-high $2,135/oz, silver briefly reached $25 before falling back to $19. While gold managed a 13% gain in 2023, silver was basically flat, entering the year at $23.96 and exiting it at $22.29.

Still, silver looks under-priced based on its historical relationship with gold and its supply-demand dynamics, explained in detail above.

The gold-silver ratio currently sits at 88:1, meaning it takes 88 ounces of silver to buy one ounce of gold. The ratio on the modern era has averaged about 50:1. Historically, the ratio has always returned to the mean. When it does, it often snaps back dramatically, as the chart below shows.

Economist Peter Schiff noted in a recent podcast that, while gold set a record, silver is far below its record of just under $50 an ounce.

I think silver is a particularly good buy right here because gold is at a record high and silver would have to double to hit its record high. That tells me that silver is very cheap.”

Another Peter Schiff column quotes Gregor Gregersen, the CEO of Silver Bullion Pte Ltd., stating that silver mine production has fallen due to a lack of investment:

“Production cannot be materially increased over the short term as it can take over 10 years to commence new mining operations. Therefore, increased silver prices will not lead to increased mine production for a long time.”

We’ve already said the incentive price for silver is too low. Now, Gregersen is saying even if silver goes higher, there will be a lag before we see an increase in mine supply. Meanwhile, the demand for silver and all its industrial (and monetary) applications will continue to increase, exacerbating the silver supply deficit.

Higher demand without a corresponding increase in supply practically guarantees a higher silver price.

Gregersen “was intrigued by unofficial chatter about upcoming silver scarcities due to rapidly growing photovoltaic demands” during the Asia Pacific Precious Metals Conference.

He summed up his column by stating that Photovoltaic demand is poised to drain global physical reserves of silver. Should the 2024 production capacity reach 1,000 GW as predicted by IEA, the required photovoltaic silver demand would likely surpass 500 million troy ounces of silver by mid-decade. It is very unlikely that such demand could be satisfied without drastically higher silver prices or much higher physical metal premiums.”

Conclusion

While silver is an industrial metal, more fundamentally, as Schiff reminds us, it is also a monetary metal:

Despite being more volatile in the short term, silver tends to track with gold over time. Historically, it has outperformed gold in a gold bull market.

At some point, investors will have to reckon with the shrinking supply of silver coupled with rising demand, along with the Fed’s inability to bring inflation back to its 2% target. When that happens, the price of silver will likely take off. If it does, $25 silver will look like a real bargain.

Richard (Rick) Mills

aheadoftheherd.com

subscribe to my free newsletter

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.

Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.

Any AOTH/Richard Mills document is not, and should not be, construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.

AOTH/Richard Mills has based this document on information obtained from sources he believes to be reliable, but which has not been independently verified.

AOTH/Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness.

Expressions of opinion are those of AOTH/Richard Mills only and are subject to change without notice.

AOTH/Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission.

Furthermore, AOTH/Richard Mills assumes no liability for any direct or indirect loss or damage for lost profit, which you may incur as a result of the use and existence of the information provided within this AOTH/Richard Mills Report.

You agree that by reading AOTH/Richard Mills articles, you are acting at your OWN RISK. In no event should AOTH/Richard Mills liable for any direct or indirect trading losses caused by any information contained in AOTH/Richard Mills articles. Information in AOTH/Richard Mills articles is not an offer to sell or a solicitation of an offer to buy any security. AOTH/Richard Mills is not suggesting the transacting of any financial instruments.

Our publications are not a recommendation to buy or sell a security – no information posted on this site is to be considered investment advice or a recommendation to do anything involving finance or money aside from performing your own due diligence and consulting with your personal registered broker/financial advisor.

AOTH/Richard Mills recommends that before investing in any securities, you consult with a professional financial planner or advisor, and that you should conduct a complete and independent investigation before investing in any security after prudent consideration of all pertinent risks. Ahead of the Herd is not a registered broker, dealer, analyst, or advisor. We hold no investment licenses and may not sell, offer to sell, or offer to buy any security.