Companies

$2.8B for US #BatteryMetals #supplychain Announced

2022.10.20

Twenty days before the midterm elections, the Biden administration has made a major funding announcement regarding electric vehicles. In Washington…

![]()

2022.10.20

Twenty days before the midterm elections, the #Biden administration has made a major funding announcement regarding #ElectricVehicles. In Washington on Wednesday, the President said the Department of Energy will award $2.8 billion in grants to 20 manufacturing and processing companies for projects across 12 states.

The funding will come from the bipartisan infrastructure law passed last year and will include components affecting both the electric grid and electric vehicles, CNN reported.

The 12 states include Alabama, Georgia, Kentucky, Louisiana, Missouri, Nevada, New York, North Carolina, North Dakota, Ohio, Tennessee and Washington — some of which, like Georgia, Kentucky and Tennessee, already have battery plants in the works.

The projects are expected to “develop enough lithium to supply over 2 million electric vehicles annually and establish significant domestic production of graphite and nickel,” according to a fact sheet.

The private sector present at Wednesday afternoon’s event is expected to match the government’s investment, leveraging the $2.8B for a total investment of $9 billion.

White House officials emphasized the intent of the funding is to narrow the lead China has over the United States when it comes to the mining and processing of critical minerals.

“Over the last decades, China has cornered the supply chain for batteries from critical mineral mining and processing to cathode anode belt manufacturing for critical minerals. For the critical minerals lithium, cobalt, graphite, nickel and manganese that are crucial to advanced batteries, China controls nearly all global processing capacity,” an official said, adding, “As the world transitions from a fossil fuel to a clean energy-powered economy, we cannot trade dependence on oil from autocrats like Putin to dependence on critical minerals from China.”

In this graphite-focused article, we’re taking a deep dive into all the plans for lithium-ion battery plants in the United States over the next few years, and the amount of graphite they would require.

Electrification

The move away from fossil-fuel-powered vehicles to EVs run on batteries is happening in almost every country. Governments are spending billions on EV charging infrastructure and subsidies to incentivize consumers to switch to hybrids and plug-in electric cars, vans and trucks. China is the leader but other countries are catching up, as large automakers like Volkswagen, Mercedes-Benz, GM and Ford come out with new EV models and plan new EV manufacturing/ assembly plants in North America and Europe.

The electrification of the global transportation system doesn’t happen without lithium and graphite needed for lithium-ion batteries that go into electric vehicles.

Graphite is included on a list of 23 critical metals the US Geological Survey has deemed critical to the national economy and national security.

An average plug-in EV has 70 kg of graphite. Every 1 million EVs requires about 75,000 tonnes of natural graphite, equivalent to a 10% increase in flake graphite demand.

A White House report on critical supply chains showed that graphite demand for clean energy applications will require 25 times more graphite by 2040 than was produced in 2020.

It’s thought that battery demand could gobble up well over 1.6 million tonnes of flake graphite per year (out of a 2021 market, all uses, of 1Mt). Remember, the mining industry still needs to supply other graphite end-users. Currently, the automotive and steel industries are the largest consumers of graphite with demand across both rising at 5% per annum.

US graphite dependence

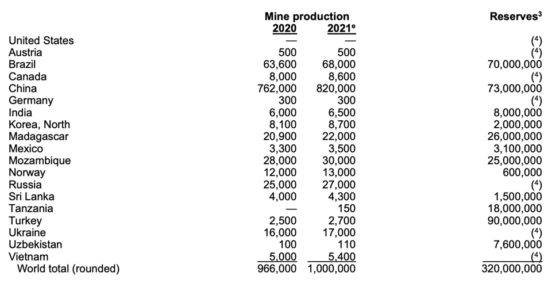

The US could be left in the dust as it continues to play catch-up in the EV race. For starters, natural graphite material is very difficult to source. Only about 20 countries make up the world’s supply, many of which produce insignificant amounts (<10,000 tonnes a year).

China is by far the biggest producer with nearly 80% of the world’s graphite production. Due to weak environmental standards and low costs, China also controls almost all graphite processing, establishing itself as a dominant player in every stage of the supply chain.

After China, the next leading graphite producers are Brazil, Mozambique, Russia and Madagascar. The US, on the other hand, produces absolutely no graphite, and therefore must rely solely on imports to satisfy domestic demand.

A burgeoning EV sector has meant that the level of import dependence has increased over the years. From 2016 to 2018, US graphite imports nearly doubled from 38,900 tonnes to 70,700 tonnes. Although imports have leveled off in recent years, the numbers are still substantial and alarming for the future of America’s EV economy.

According to the USGS, in 2021 the US imported 53,000 tonnes of natural graphite, of which about 57% was flake and high-purity, 42% amorphous, and 1% lump and chip graphite. The top importers were China (33%), Mexico (21%), Canada (17%) and India (9%).

But taking into account the fact that China, its main competition, controls all graphite processing, the US is actually not 33% dependent on China for its battery-grade graphite, but 100%. This is a precarious position to be in should it wish to stay in contention for EV dominance, and it will only worsen as demand for battery minerals grows.

Government funding

Fortunately, the US government has begun taking a stand on US critical minerals vulnerability, including graphite.

On February 24, 2021, President Joe Biden signed an executive order aimed at strengthening critical US supply chains. Graphite was identified as one of four minerals considered essential to the nation’s “national security, foreign policy and economy.”

This year, the United States government invoked its Cold War powers by including lithium, nickel, cobalt, graphite and manganese on the list of items covered by the 1950 Defense Production Act, previously used by President Harry Truman to make steel for the Korean War.

To bolster domestic production of these minerals, US miners can now gain access to $750 million under the act’s Title III fund, which can be used for current operations, productivity and safety upgrades, and feasibility studies. The decision could also cover the recycling of these materials, according to Bloomberg sources.

The Biden administration has also allocated $6 billion as part of the $1 trillion infrastructure bill — towards developing a reliable battery supply chain and weaning the auto industry off its reliance on China, the biggest EV market and leading producer of lithium-ion cells.

All of this is in addition to the $2.8B funding announcement on Oct. 19.

The Biden administration’s plan is to have 50% of US auto production be electric and hybrid by 2030.

Battery plants galore

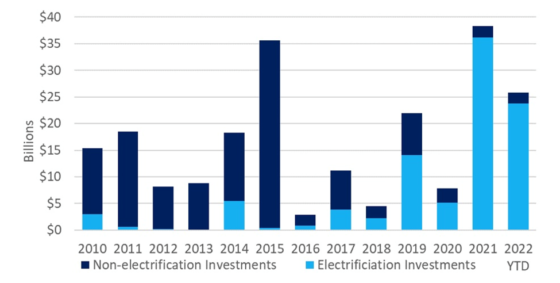

According to data collected by The Book of Deals, via cargroup.org, in 2021 automakers announced $36 billion of investments to build facilities dedicated to manufacturing EVs and batteries. In the first five months of 2022, automakers announced $24 billion in EV-related investments, almost double the investments announced by the same time last year. Recent automaker announcements on EV and battery manufacturing investments demonstrate an acceleration of growth in the EV market driven by new government EV targets and increasing consumer demand.

State-directed funding for vehicle electrification has been made available through President Biden’s American Rescue Plan, a $1.9 trillion funding package to help US states, territories, cities and tribal governments replace tax revenue lost during the pandemic. According to a recent Bloomberg piece, hundreds of billions in federal aid was made available to states but never spent.

Michigan took advantage by announcing a $6.6 billion electric-truck factory and battery plant from General Motors, along with a billion in corporate subsidies. The announcement came soon after rival Ford made public that it had chosen two southern states, Tennessee and Kentucky, as sites for an $11 billion electric-vehicle project.

The Bloomberg article quotes an expert saying that, while states have long competed against one another to lure companies, the scale and the ferocity of it now — for EV plants, semiconductor factories and other megaprojects — are unprecedented.

“I have never seen the same kind of surge in subsidies all across the US all happening at the same time,” said Michael Farren, a senior researcher at the Mercatus Center at George Mason University and a critic of corporate incentives. “It’s pretty clear that there’s an external motivating factor, and that is the American Rescue Plan relief funds.”…

The $350 billion that Congress set aside for states and municipalities in May 2021 is coinciding with a once-in-a-century transformation of the auto industry, as carmakers prepare to retire the combustion engine in favor of battery power…

What is known is that global carmakers and established battery manufacturers have announced plans to invest at least $50 billion into at least 10 states to build EV assembly and battery plants since the start of 2021, and states have made commitments totaling at least $10.8 billion to lure those investments, according to a tally of publicly disclosed incentives by Bloomberg and Good Jobs First. That figure almost certainly underestimates the actual number.

Arun Kumar, a managing director at consulting firm AlixPartners, forecasts a 54% EV market share globally by 2035, and suggests that at such volumes, more EV plants will be coming to the United States.

Tennessee and Georgia exemplify how state-corporate collaboration is working to create the downstream part of a critical minerals supply chain. At Blue Oval City, a six-square-mile site an hour’s drive from Memphis, an assembly plant is being built to produce Ford’s new electric F-150 pickup, and a battery plant that together promise to create nearly 6,000 jobs. State officials say the $5.6B project will add $3.5B annually to Tennessee’s economy. A cash grant from the state legislature totals at least $2.4 billion, which includes tax breaks, donated land, infrastructure improvements and short-term wage subsidies from the federal government, according to contract documents obtained by Bloomberg.

In June, Volkswagen America opened a $22 million Battery Engineering Lab, a 32,000-square-foot facility located next to its Chattanooga, TN plant. ABC News said the company’s compact ID.4 SUV, currently imported from Germany, will roll off assembly lines for US consumers later this year. VW has reportedly invested more than $800 million to prepare its Chattanooga plant for the local assembly of the ID.4 SUV in 2022.

Georgia, meanwhile, has landed two $5B EV deals from Rivian and Hyundai. The state offered incentives worth $3.3B to win the projects, which promise to create over 15,000 jobs.

Mercedes-Benz’s Bibb County, Alabama plant joins the carmaker’s global battery production network with factories on three continents. The German company has said it will go all-electric by 2030, with plans invest 40 billion euros into BEVs from 2022-30.

Rival BMW in 2019 expanded its battery facility at Plant Spartanburg, South Carolina, more than doubling capacity. According to ABC News, Higher performing, fourth-generation batteries are assembled on-site for the BMW X5 and BMW X3 plug-in hybrid electric variants and 120 employees were specially trained to work the new line, having completed an extensive program in battery production, robotics and electrical inline quality inspection along with end-of-line testing, BMW said.

Of course we can’t forget about Tesla, the country’s top seller of EVs. The company produces batteries and electric motors for the Model 3, at is Sparks, Nevada plant, which broke ground in 2014. The company says the site currently produces more batteries in terms of kilowatt-hours than all other carmakers combined.

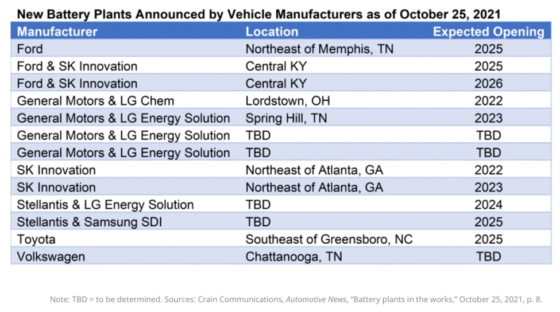

As for future developments, 13 electric-vehicle battery factories are planned in the United States between 2021 and 2026, according to the table below by the Department of Energy. This is in addition to battery plants that are already in operation. Of the 13 new plants, eight are joint ventures between automakers and battery manufacturers. Many will be located in the US Southeast or Midwest.

Fourth down on the list, General Motors and Korean battery-maker LG Chem are teaming up to build three US EV battery factories with a $2.5 billion loan from the US Department of Energy. Known as Ultium Cells, the joint venture will open a new 2.8 million-square-foot facility in Lansing, Michigan, its third battery cell manufacturing plant in the country. Workers will supply battery cells to Orion Assembly in Michigan and other GM EV assembly plants. Production at the Ohio plant was to begin in August, with the Tennessee plant expected to open in late 2023 and the Michigan plant in 2024.

Another JV, between Stellantis and Samsung SDI, plans to build an EV battery plant in Kokomo, Indiana, targeting a 2025 launch with a total investment of $2.5B.

Stellantis also announced a $4 billion investment with LG Energy Solution to build an EV battery plant in Windsor, Ontario.

Tesla supplier Panasonic earlier this year announced it will build a new lithium-ion battery factory in De Soto, Kansas. Reuters said the $4 billion plant will mostly supply batteries to Tesla, but not exclusively.

Hyundai recently said it plans to spend $5.5 billion to build facilities for manufacturing EVs and batteries in Savannah, Georgia, making it the automaker’s first EV-only plant in the United States.

Graphite calculation

With all that is going on, it’s easy to lose sight of the big picture. The Center for Automotive Research provides some perspective.

The marketshare of all EVs, including full electrics, hybrids and fuel cell (hydrogen) vehicles, amounted to 12.2% in the first half of 2022, compared to 11.9% in 2021. If Biden’s targeted one-half of new light-duty vehicles being battery-electric and plug-in by 2030, is fulfilled, it would require roughly 8 million new EV batteries a year.

Have we got the metals, and in particular, the graphite?

An average plug-in EV has 70 kg of graphite. Every 1 million EVs requires 70,000,000 kg (70,000 metric tonnes) of natural graphite.

70,000 tonnes X 8 (million) = 560,000 tonnes

In 2021 the US imported 53,000 tonnes of natural graphite, of which about 57% was flake and high-purity, 42% amorphous, and 1% lump and chip graphite. For round numbers, let’s say 50%, or $26,500 tonnes of battery-grade graphite, was imported (only high-purity flake graphite is suitable for EVs).

Getting from 26,500t to 560,000 tonnes would require a 21X increase in the amount of graphite the United States either imports or produces domestically. There are currently no producing US graphite mines and all of the country’s graphite processing is done overseas.

I pose a simple question: Where are we going to find the graphite?

Graphite One (TSXV:GPH, OTCQX:GPHOF)

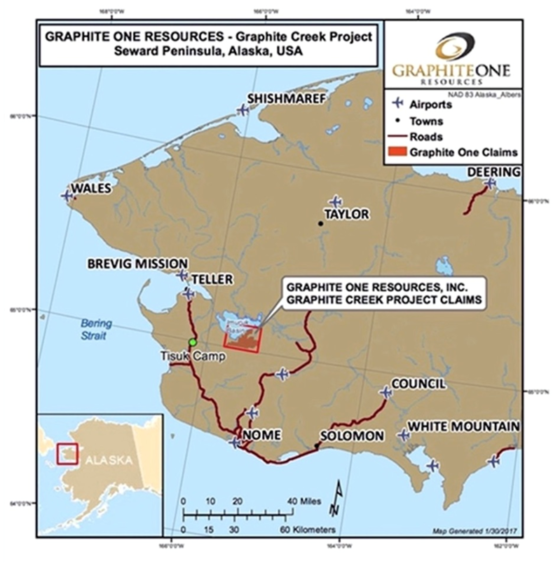

Fortunately, there is a potential solution to the problem, in a large graphite mine being developed in Alaska.

The Graphite Creek property is situated along the northern flank of the Kigluaik Mountains, Alaska, spanning 18 kilometers.

Located on the Seward Peninsula, Graphite Creek in early 2021 was given High-Priority Infrastructure Project (HPIP) status by the Federal Permitting Improvement Steering Committee (FPISC). The HPIP designation allows Graphite One to list on the US government’s Federal Permitting Dashboard, which ensures that the various federal permitting agencies coordinate their reviews of projects as a means of streamlining the approval process.

In other words, having HPIP means that Graphite Creek will likely be fast-tracked to production, while of course adhering to the necessary regulations that are integral to developing any new mine in the US.

The US Geological Survey has cited Graphite Creek as the largest known graphite deposit in the country.

The March 2019 resource estimate — derived from drilling less than 30% of the mineralization — showed 10.95 million tonnes of measured and indicated resources at a graphite grade of 7.8% Cg (graphitic carbon), for 850,000 tonnes of contained graphite. Another 91.9 million tonnes were tagged as inferred resources, with an average grade of 8.0% Cg containing 7.3 million tonnes.

In the prefeasibility study there is a marked increase in mineral resources and reserves after incorporating the results from 2021 drilling.

66 holes were completed in the resource area for a total of 10,112 meters. The resource data base consists of 6,412 assays. The resource remains open down dip and along strike to the east and west.

According to Graphite One, the drill results continue to show consistent, near-surface high-grade intercepts with numerous holes returning grades higher than 10% and up to 35.78% graphitic carbon. In fact they suggest three times the strike length of the existing resource.

The Graphite Creek Mine would produce, on average, 51,813 tonnes per year of graphite concentrate for its projected 23-year mine life. (At an average grade of 5.6% Cg and a strip ratio of 2.2:1, that works out to 22.5Mt over 23 years. It is expected that peak mine production will be approximately 11,000 tpd).

The deposit would be mined with conventional open-pit mining methods including drilling, blasting, loading and hauling. The strip ratio is 2.2:1 using an ore cut-off grade of 2% graphitic carbon and an average head grade of 5.6% graphitic carbon. The pit would be mined in six phases over 24 years. One year of pre-stripping would occur prior to the start-up of the process facility. Under the PFS plan, ore would be hauled to the facility, to be built adjacent to the pit. Run-of-mine waste would be co-mingled with dewatered process tails and placed in waste dumps.

The process facility would process an average of 2,860 tonnes per day (tpd) for 365 days per year. The flowsheet design is based on metallurgical test work conducted at SGS Canada’s facilities at Lakefield, Ontario.

On August 16, 2022, the United States enacted the Inflation Reduction Act, which instituted, among other things:

- A tax credit to producers in the U.S. of anode materials equal to 10% of the costs incurred with respect to the production of anode materials commencing December 31, 2022 and reducing to 75%, 50%, 25%, and 0% in 2030, 2031, 2032 and thereafter, respectively.

- A tax credit equal to 10% of the costs incurred with respect to production of graphite purified to a minimum purity of 99.9 percent graphitic carbon by mass (“purified graphite”) – the phase out provisions set out above do not apply.

- Only production in the United States qualifies for the tax credit.

Graphite One’s production is expected to qualify under the act for tax credits in both categories as it plans to produce both anode materials and purified graphite in the United States.The company will evaluate the act’s impact on the PFS economics and announce the results when available. GPH says the impact is expected to improve upon the post-tax results, which showed a 22% IRR, using an 8% discount rate, with net present value of $1.36 billion and a payback period of 5.1 years.

Graphite One has a “parallel strategy” to simultaneously develop a battery anode materials manufacturing facility in Washington State and the Graphite Creek Mine in Alaska. Combined they are known as the Graphite One Project. Manufacturing would begin with purchased materials until Alaska production is available.

The company aims to become the first vertically integrated domestic producer to serve the nascent US electric vehicle battery market.

The Vancouver-headquartered company in April announced a memorandum of understanding (MOU) with Sunrise (Guizhou) New Energy Material Co., Ltd., a lithium-ion battery anode producer based in Guizhou Province, China.

The report “Lithium-Ion Battery Anode Market by Materials (Active Anode Materials and Anode Binders), Battery Product (Cell and Battery Pack), End-Use (Automotive and Non-Automotive), and Region (Europe, North America, and Asia Pacific) – Global Forecast to 2026″, reports the market size of the lithium-ion battery anode market was estimated at USD 8.4 billion in 2021 and is projected to reach USD 21.0 billion by 2026, growing at a CAGR of 19.9%.

Sunrise and GPH plan to form an alliance to establish a graphite material manufacturing facility in Washington State. The MOU’s term was recently extended and Sunrise is in the process of preparing anode materials for sample purposes from Graphite Creek concentrate produced from graphite recovered during exploration.

The third link in Graphite One’s US-based graphite supply chain involves battery materials recycler Lab 4 Inc. of Nova Scotia, Canada. Under an earlier MOU, GPH and Lab 4 will work collaboratively to design and build a recycling facility for end-of-life EV and lithium-ion batteries. Lab 4 provides laboratory and engineering support to mining companies with a focus on recycling graphite, manganese and other minerals.

According to Fortune Business Insights, the global Lithium-ion Battery Recycling market size is projected to grow from USD 1.70 billion in 2020 to USD 6.55 billion in 2028, at CAGR of 18.5% during forecast period

The recycling facility will be located next to the Washington State manufacturing facility and engineered to accept used EV batteries for feedstock.

On Aug. 29 GPH announced an up-size of its previously posted $15.525 million non-brokered private placement, to $21.275 million. Up to 18,500,000 units will be issued and offered for $1.15 per unit.

This follows a shares-for-debt arrangement reported between Graphite One and Taiga Mining Company, Inc. Relieved of its debt obligations, and a private placement in the offing that could fill Graphite One’s coffers with up to $21.2 million, I feel confident about the company’s financial wherewithal to advance the Graphite One Project through to its next stage of development, a feasibility study.

When the extremely positive pre-feas is combined with the political support behind the project, and the fact that graphite is a critical mineral currently with zero production in the US, which is 100% dependent on China, for future battery-grade graphite requirements 22X greater than current import levels and it’s circular economy approach – mine, manufacture, recycle – Graphite One is Ahead of the Herd’s pick in the graphite space going forward.

Graphite One Inc.

TSXV:GPH, OTCQX:GPHOF

Cdn$1.15, 2022.10.19

Shares Outstanding 83.3m

Market cap Cdn$121.7m

GPH website

Richard (Rick) Mills

aheadoftheherd.com

subscribe to my free newsletter

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.

Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.

Any AOTH/Richard Mills document is not, and should not be, construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.

AOTH/Richard Mills has based this document on information obtained from sources he believes to be reliable, but which has not been independently verified.

AOTH/Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness.

Expressions of opinion are those of AOTH/Richard Mills only and are subject to change without notice.

AOTH/Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission.

Furthermore, AOTH/Richard Mills assumes no liability for any direct or indirect loss or damage for lost profit, which you may incur as a result of the use and existence of the information provided within this AOTH/Richard Mills Report.

You agree that by reading AOTH/Richard Mills articles, you are acting at your OWN RISK. In no event should AOTH/Richard Mills liable for any direct or indirect trading losses caused by any information contained in AOTH/Richard Mills articles. Information in AOTH/Richard Mills articles is not an offer to sell or a solicitation of an offer to buy any security. AOTH/Richard Mills is not suggesting the transacting of any financial instruments.

Our publications are not a recommendation to buy or sell a security – no information posted on this site is to be considered investment advice or a recommendation to do anything involving finance or money aside from performing your own due diligence and consulting with your personal registered broker/financial advisor.

AOTH/Richard Mills recommends that before investing in any securities, you consult with a professional financial planner or advisor, and that you should conduct a complete and independent investigation before investing in any security after prudent consideration of all pertinent risks. Ahead of the Herd is not a registered broker, dealer, analyst, or advisor. We hold no investment licenses and may not sell, offer to sell, or offer to buy any security.

Richard owns shares of Graphite One Inc. (TSXV:GPH). GPH is a paid advertiser on his site aheadoftheherd.com

tsxv otcqx ax lithium cobalt manganese nickel tsxv-gph graphite-one-inc

Dolly Varden consolidates Big Bulk copper-gold porphyry by acquiring southern-portion claims – Richard Mills

2023.12.22

Dolly Varden Silver’s (TSXV:DV, OTCQX:DOLLF) stock price shot up 16 cents for a gain of 20% Thursday, after announcing a consolidation of…

GoldTalks: Going big on ASX-listed gold stocks

Aussie investors are spoiled for choice when it comes to listed goldies, says Kyle Rodda. Here are 3 blue chips … Read More

The post GoldTalks: Going…

Gold Digger: ‘Assured growth’ – central bank buying spree set to drive gold higher in 2024

Central banks will drive the price of gold higher in 2024, believe various analysts Spot gold prices seem stable to … Read More

The post Gold Digger:…