Uncategorized

How to Build a Crisis-Proof, Inflation-Proof Portfolio

A step-by-step plan that will grow your wealth during good times… and protect it during bad times.

Every year, U.S. News & World Report produces…

A step-by-step plan that will grow your wealth during good times… and protect it during bad times.

Every year, U.S. News & World Report produces a list of what it calls the “Best Places to Live in the U.S.”

To create the list, the magazine evaluates more than 100 metro areas in terms of job market, natural surroundings, home affordability, crime rate, school quality, and other aspects.

Nearly every year, Colorado Springs, Colo., ranks at or near the top of the list.

Nestled against the Rocky Mountains and featuring plenty of green space, Colorado Springs offers “mountain living” at its finest… which is why the city has enjoyed constant population growth since 1960 and become a media darling.

Source: Neil Podoll/ShutterStock.com

Source: Neil Podoll/ShutterStock.com

Colorado Springs doesn’t just attract people who like mountain views.

In the 1950s – during the height of the Cold War – the U.S. military picked Colorado Springs to be the home of the world’s most important, most powerful, most secure military command post.

In the wake of World War II, U.S. leaders were worried about nuclear war with the Soviet Union. The military decided it needed an ultra-safe, ultra-secure base from which it could command America’s nuclear arsenal.

After a long nationwide study, they selected Colorado Springs because of its distance from the coasts (attacking missiles or bombers would have to fly a very long way)… because it’s the most seismic-sound region of Colorado (no earthquakes)… and because it’s next to a giant mass of granite named Cheyenne Mountain.

The military knew it could bury its command center below thousands of feet of Cheyenne’s solid rock… and make it able to withstand any kind of attack, including a nuclear one.

Starting in 1961, the U.S. Army Corps of Engineers began excavating hundreds of thousands of tons of rock from under Cheyenne Mountain. Inside, they built a complete military command center shielded by more than 2,000 feet of granite.

The entrance of the facility – called the Cheyenne Mountain Complex – is protected by giant 25-ton steel doors. The buildings inside sit on massive steel springs that could absorb the shock of a nuclear blast.

At its peak, more than 1,000 military personnel manned the Cheyenne Mountain Complex. It had huge stores of water, fuel, and food. It had its own electrical plant. These attributes made the facility self-sufficient in case of national emergencies. (Today, the Cheyenne Mountain Complex serves as NORAD and U.S. Northern Command’s Alternate Command Center as well as a training site.)

The Cheyenne Mountain Complex is an ultra-secure, ultra-safe example of what military experts call a “hardened” structure.

The term hardened appears frequently in military planning. Hardened structures are buildings – often built underground – that are highly fortified and resistant to attacks. They’re the most fortified structures on the planet.

Hardened structures are often wrapped in thick layers of rock, concrete, and steel. They are bomb proof.

The Cheyenne Mountain Complex is hardened like no other structure on Earth.

It is nuclear bomb proof.

Source: Photo from Norad.mil

Source: Photo from Norad.mil

If the past 30 years of history have taught us anything, it’s that we all need to “harden” our financial lives and investment portfolios. We all want our money protected by the financial equivalent of the Cheyenne Mountain Complex.

Just think about it…

In 2020, we lived through the worst pandemic in a century… one that brought economic lockdowns that hit the world like a meteor from space.

And it wasn’t long ago that we lived through the Great Recession of 2007-’08… and the bursting of the 2000 tech bubble.

We’ve seen once-dominant businesses like Eastman Kodak and Sears go bankrupt.

We’ve seen “flash crashes” … we’ve seen Enron revealed as a fraud… we’ve seen Bernie Madoff busted for running a giant pyramid scheme… we’ve been lied to by hundreds of high-profile politicians, reporters, and CEOs.

Source: InvestorPlace.com

Source: InvestorPlace.com

We also live in a world rife with cybercrime and financial scams.

In a perfect world, we could invest our money into a simple and safe stock fund and earn 12% a year with little volatility for decades.

But we don’t live in a perfect world.

We live in a world where stock market crashes, wars, and pandemics occur with disturbing regularity.

We live in a world where criminals prey upon the unsuspecting.

We live in a world where governments bungle their financial affairs and make shortsighted decisions.

For these reasons, we live in a world where building and maintaining a “hardened” financial life is one of the smartest moves you can make for yourself and your family.

Your ability to earn money, save money, and grow your savings should be as safe and secure as the Cheyenne Mountain Complex.

As one of the world’s largest investment research firms, InvestorPlace hand selects and recommends many stocks and bonds each year for purchase by investors.

However, the world’s best individual stock and bond ideas aren’t worth much if they don’t fit inside a robust wealth management framework that provides you a great mix of safety and potential upside.

Every smart investor’s goal should be the construction and ownership of a crisis-proof, inflation-proof portfolio that can make you money during the good times… and keep you safe during the bad times.

Inside this report, you’ll find step-by-step instructions for building just such a hardened, all-weather portfolio.

Some Assets “Zig” When Stocks “Zag”

According to the investment bank Credit Suisse, U.S. stocks have returned an average of about 10% per year for the past 120 years.

This average return beats gold, oil, bonds, cash, and every other widely traded financial asset on the market.

Stocks produce excellent long-term returns for a simple reason: The U.S. system of free enterprise leads to tremendous wealth creation. It gives life to value-creating businesses like Apple, Ford, Starbucks, Home Depot, Coca-Cola, Nike, Microsoft, Boeing, and Google.

Free people and free markets create goods and services that people want to buy – and wealth follows. Investors go along for the ride.

Given the stock market’s long track record of success, it’s no wonder many people are interested in stocks.

However, the high returns you can earn in stocks come with a tradeoff…

Stocks are more volatile than bonds and many other assets. From time to time, stocks experience big declines in value (aka “bear markets”).

For example, during the 2000-’02 bursting of the technology stock bubble, the benchmark S&P 500 index declined by 49%.

Then you have the stock bear market that accompanied the Great Recession of 2007-’08. Stocks fell an incredible 56% during the decline.

These two recent examples show that while generating excellent long-term gains, stocks can inflict serious short-term pain.

That risk is more than many people are comfortable taking on.

And no crisis-proof “hardened” portfolio should decline in value by 56%.

Fortunately for investors, some assets “zig” when stocks “zag.”

They do well even when the stock market is struggling.

The world is a big place. The menu of assets we as investors can own is large and varied.

There’s rental real estate. There’s farmland. There’s timberland. There’s gold and government bonds. There’s municipal bonds and corporate bonds. There’s cash, commodities, collectibles, and currencies. There’s private business. And, of course, there’s cryptocurrency, like Bitcoin.

Different economic climates affect the price of these assets differently.

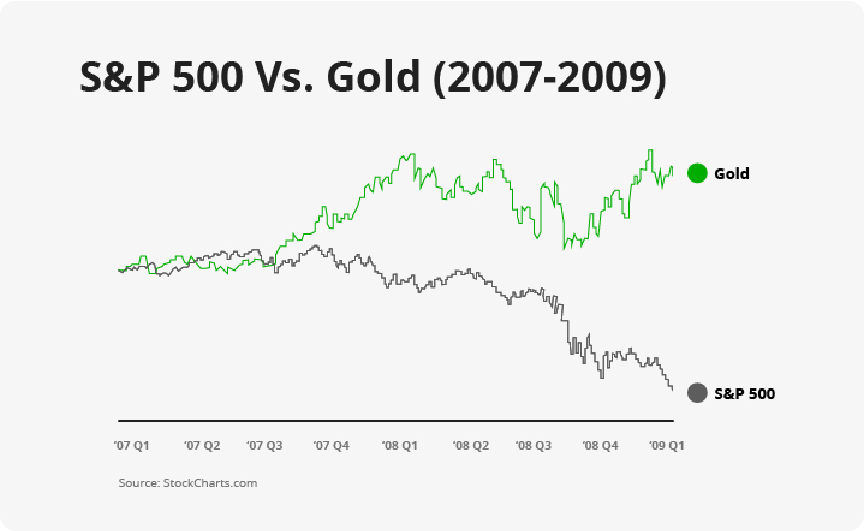

For example, in 2007, stocks began to decline in advance of the Great Recession.

As the crisis began to take hold, stocks fell throughout 2007, 2008, and 2009. The broad market fell 51.7% from its 2007 high to its 2009 low.

During that terrible period for stocks, gold – which is traditionally a “safe haven” asset – gained 27.8% You can see this big difference in returns in the chart below:

Source: StockCharts.com

Source: StockCharts.com

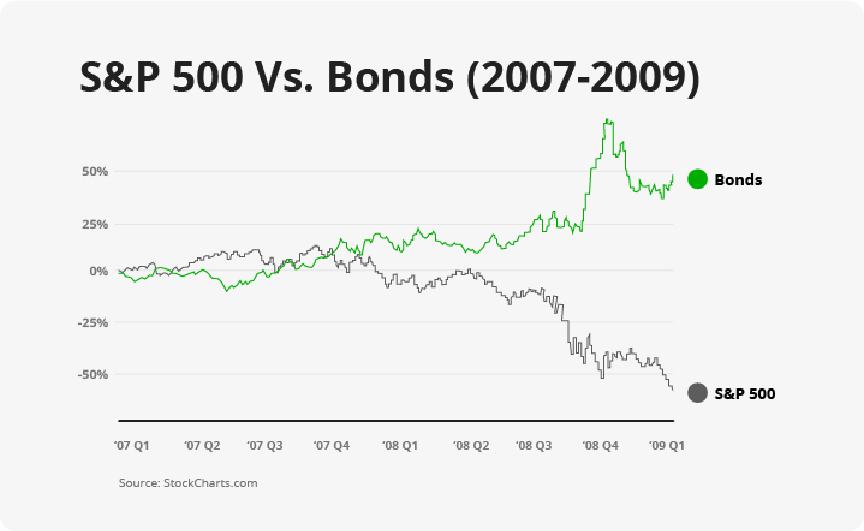

During the same rough period for stocks, government bonds – another traditional safe haven – climbed about 18%.

You can see this big difference in returns in the chart below:

Source: StockCharts.com

Source: StockCharts.com

Or consider what happened during the 2000-’02 bursting of the tech bubble and the subsequent bear market in stocks.

During this brutal time for investors – where technology stocks lost over 70% of their value – corporate bonds returned 9.3% in 2000… 7.8% in 2001… and 12.1% in 2002.

Real estate also did well during the tech meltdown. The S&P Case-Shiller U.S. National Home Price Index increased 27% from Jan. 1, 2000, through the end of 2002.

You see these kinds of divergent returns across asset classes over and over and over throughout history.

Because different economic climates affect different businesses and asset classes differently, some assets “zig” when stocks “zag.”

That’s why an investor focused on building and maintaining a crisis-proof financial life will own a diversified mix of assets.

For people who want to build crisis-proof, hardened financial lives this is where something called “asset allocation” comes into play.

Smart Asset Allocation: They Key to Building a Hardened Portfolio

In the investment world, the art of “stock picking” gets the most press.

The financial media constantly reports on individual companies and their stock prices. People love to learn about interesting stocks with huge potential. After all, it’s exciting and fun.

However… when it comes to successful investing and building wealth safely, asset allocation is 100 times more important than stock picking.

Asset allocation is the part of your investment strategy that dictates how much of your wealth you place in broad asset classes like stocks, bonds, cash, commodities, precious metals, and real estate.

Over the course of your career as an investor, asset allocation will have a much, much greater impact on your wealth than stock picking will.

The ratio will be at least 100 to 1.

Many individual investors focus much of their time and energy on stock picking. They don’t spend any time learning what sensible asset allocation is. As a result, they take crazy risks with their savings.

However, investors interested in having a “hardened” financial life are very focused on asset allocation.

The most important aspect of asset allocation is using it to diversify your holdings across private businesses, public stocks, real estate, precious metals, cash, commodities, insurance, and other financial vehicles.

Ideally, you want a mix of assets that greatly limits your exposure to a big decline in one asset class.

Intelligent asset allocation means you DON’T bet the farm on a single stock or a single asset class.

For example, many of us can recall the catastrophic losses suffered by some employees of Enron.

In the late 1990s, many investors considered Enron the world’s most innovative company. Its executives were the superstars of Corporate America.

So, some Enron employees placed all their retirement savings in Enron stock.

Their asset allocation was “100% Enron.”

When Enron was revealed as one of the biggest frauds in American history, its stock went to zero.

The employees who bet the farm on Enron were completely wiped out.

These people used absolutely horrible, incredibly risky asset allocation.

Or consider people who went “all in” on real estate in 2005 and 2006.

Back then, the U.S. real estate mania was in full force. Real estate was considered a “can’t lose” bet.

So, many people put all their savings into real estate… and even took on loads of debt to “leverage” their returns.

When the real estate market crashed, it wiped out these “all in” real estate players.

Source: iStockphoto

Source: iStockphoto

Absolutely crazy asset allocation was the heart of their downfall.

They bet the farm on one asset class… and that asset class was in a bubble.

If you keep a huge portion of your wealth in one stock or a single asset class – whether it’s stocks, bonds, oil, gold, or real estate – you leave yourself exposed to a large decline in the value of that asset class.

You make yourself financially “fragile”… the opposite of hardened.

Given the big risks that going “all in” on one stock or one asset class presents, it makes great sense to diversify your wealth.

Think of it like eating a balanced diet.

You want to include options from different food groups. Taken together, a mix of things helps you achieve maximum health.

In the next section, we’ll cover what options we have on the investment menu. Let’s jump right in…

Harden You Portfolio: Your Investment Menu

Stocks

As we covered earlier, stocks are one of the most popular investments in America… for good reason.

When you buy a share of stock, you buy a fractional ownership stake in a real business, like home improvement chain Home Depot, automaker Ford, or online retailer Amazon.

By owning stocks, you directly participate in economic growth and productive enterprise. Over the past 120 years, stocks have returned an average of about 10% per year. This beats every other kind of widely available investment.

Remember, stocks have generated these excellent long-term returns despite world wars… the Great Depression… government shutdowns… political upheavals… the Cuban Missile Crisis… and every other crisis you can think of.

As I mentioned above, the high returns you can make in stocks comes with tradeoffs: volatility and bear markets. If your career as a stock investor spans a few decades, you are virtually guaranteed to live through several serious bear markets where stocks fall at least 20%.

Still, if you can accept that volatility in exchange for higher long-term returns, stocks always deserve serious consideration for your portfolio.

Bonds

Bonds are another popular investment, especially among conservative investors. A bond is essentially a loan made by an investor to a borrower. Borrowers can be companies, states, or governments… just to name a few.

When you purchase a bond from a borrower you are lending them money to fund a project. For example, governments will use money from the sale of bonds to help build roads or schools.

In return, as an investor, you’ll be paid income through interest payments. (Interest rates on bonds can be fixed or variable.) Plus, you have the “guarantee” that by a certain date (the maturity date) you will be paid back your initial investment.

Bonds are sold on the public markets and are considered a fixed-income investment. As we mentioned above, one of the biggest benefits to bonds is you will typically receive income through interest payments.

That being said, the average return on a bond investment is much lower than stocks. And if a bond you hold has a variable yield, there is a risk that the yield, and therefore your income payment, will fall.

Bonds are not subject to the same short-term volatility that stocks can encounter. For investors that fall into the conservative camp (more on that a little later), bonds create a great source of reliable income.

Gold

Gold has been considered “money” for more than 2,000 years. It’s divisible, doesn’t rust or crumble, can be transported fairly easily, and, maybe most importantly, can’t be created by governments.

Because of this, during times of high inflation you’ll see investors flock to gold. Gold provides a stability when the value of fiat currency is declining.

And it’s not just in times of inflation investors jump into gold. When crisis hits… when wars break out… when bank runs grip a nation… when it’s really time to just “grab the money and run,” humans keep coming back to gold.

Like we showed you earlier, during uncertain times you’ll see gold prices soar.

You can invest in gold by buying physical gold. There are even companies that facilitate the purchase and store it for you.

If buying and storing physical gold isn’t for you, another way to get exposure to the gold market is by investing in a gold ETF or public gold mining companies. (Just be aware that investing in gold miners can also experience the same volatility as the stock market.)

Gold has been considered a safe investment for thousands of years. Investing a portion of your wealth into gold will help harden your portfolio against turbulent markets.

Commodities

Commodities are raw materials used to manufacture finished goods. They can be grown, extracted, or mined.

Gold is a commodity. Other common commodities include copper, silver, coffee, corn, coal, and oil.

Like we talked about with gold, investing in commodities can be a great way to hedge against inflation and protect against the declining value of currency.

It is important to note that commodities can be affected by the geopolitical climate. We’ve seen this recently with the Russia-Ukraine war. Russia is the third-biggest exporter of oil behind the United States and Saudi Arabia. More than half of Russia’s exports go to the European Union. When Russia invaded Ukraine back in February 2022, oil prices spiked on the fear of lack of supply.

Bad for those of us at the pump. Good for anyone who had oil as part of their hardened portfolio.

With commodities, it’s important not to put all of your eggs in one basket. You want to spread your investments across different types of commodities so that you aren’t susceptible to the effects of a bad crop or an oversupply of a particular item; either could cause the price of the commodity to go down.

You can invest in a commodity by investing directly in the physical commodity, like with gold. Obviously, if you are investing in a commodity like oil, storing would be problematic. You can also get exposure to the commodity market by investing in the stock of a publicly traded commodity company or in a commodity-focused ETF.

Real Estate

Outside of owning your home, the idea of investing in real estate can be daunting for most people. But it doesn’t have to be…

When most people think of investing in real estate, they think of owning a second property and renting it out or buying and flipping houses. But unlike what HGTV would have us believe, doing either of those things will take a lot more than an occasional half hour of your time.

To invest in a physical property, you need to put in the work or pay a property management company to do so. For most people, neither is a viable option.

That said, real estate is still an attractive investment. With the right property in the right location, you can make great long-term returns while collecting monthly income (in the form of rent). There also can be tax advantages.

If that still seems like too much, not to worry,

Investors can also get exposure to the real estate market without buying a physical property through REITs. A REIT – a real estate investment trust – is a company that owns physical real estate. They can own everything from commercial and retail spaces to residential apartments buildings. REITs can be bought as easily as a stock through your preferred brokerage platform.

And, just like stocks, when you buy a REIT, you are purchasing a portion of the company and, in turn, its physical holdings. You are buying “physical” real estate without the hassle of owning it.

The best part is the federal government requires REITs to pay out 90% of their taxable income to their holders in the form of a dividend. Because of this, REITs usually pay out a higher percentage than even some of the best dividend stocks.

Bitcoin

Bitcoin was the first cryptocurrency to hit the market, in 2010, with a value of $0.0008. Now the crypto trades for tens of thousands of dollars.

Using blockchain technology, bitcoin was birthed out of the hope of creating a decentralized currency. There is a finite amount of the coins available, which need to be “mined” with complex computer programs.

Once a coin is mined, ownership can be transferred between parties through the blockchain. Today you can buy and sell bitcoin through various cryptocurrency exchanges and even some traditional brokers.

Once you purchase bitcoin, you store it in a virtual wallet.

While bitcoin hasn’t replaced traditional currency, since 2017 it has taken off as an alternative investment. Some investors even seen it as a great way to hedge downswings in the public markets.

But investing in bitcoin is not for the faint of heart. While bitcoin has been a lucrative investment for many recently, the coin endures some wild swings with the price sometimes changing thousands of dollars daily. If your investment horizon doesn’t allow for market correction, investing a significant portion of your assets in bitcoin would not be advisable.

But, as with stocks, if you can endure some short-term price swings, bitcoin could prove to be a valuable asset in your financial arsenal.

Private Investing

Until recently, investing in private companies was something only available to accredited investors… the “ultrarich.”

But with the passing of the JOBS Act of 2012, and recent rules changes from the U.S. Securities and Exchange Commission, private companies are now allowed to raise up to $5 million from nonaccredited investors.

This is great news for us. Private companies offer some of the best returns out there. The right investment can return 10X… 20X… or even 50X your money.

Just look at Peter Thiel… arguably one of the most successful venture capital investors ever. As the first outside backer in Facebook, Thiel invested $500,000 to buy a 10% stake in 2004 – a stake that would be worth more than $90 billion today.

You make money on a private company that you’ve invested in from a “trigger” or liquidity event. This is when a private company goes public through an initial public offering (IPO) or a special purpose acquisition company (SPAC) or is acquired by a larger company.

The best part is that it’s never been easier for someone to grab their share of these private companies. Just put together a list of equity crowdfunding platforms and see what looks interesting on them. Once you’ve made your choices, investing in a private company is nearly as easy as making any ecommerce transaction.

While a private company portfolio is a great addition to a diversified, hardened portfolio, there are a couple of things to keep in mind. Investing in a private company isn’t the same as buying a publicly traded stock. There isn’t a liquid market for private investments. Often your money is locked up for at least a year, and sometimes longer.

Also, the majority of startups fail, resulting in a total loss of investment. But the investments that do turn out to be winners can be spectacular and make up for the losses of many failures.

If you choose to include private companies in your hardened portfolio, you should only use expendable cash that you don’t need access to in the short term.

What Asset Allocation Mix Is Right for You?

There’s no “one size fits” all asset allocation strategy that is right for everyone.

When you (possibly with the help of a financial adviser) think about your right “mix,” you must consider your age, your risk tolerance, and your goals.

A 50-year-old who needs to pay college tuition for three children will think about asset allocation much differently than a 32-year-old with no family.

However, most of us have a similar end goals.

We’d like a diversified, hardened collection of assets that generate income… even when we are not actively working. We want to see our net worth rise during bull markets… while also not seeing our net worth decline a lot during bear markets. We want the damage inflicted by events like the Great Recession of 2008 kept to a minimum.

We want our financial life to be crisis-proof and inflation-proof.

Again, having all that means being diversified across stocks, bonds, real estate, cash, precious metals, cash, commodities, insurance, and assets like cryptocurrency and private businesses.

A Great Asset Allocation Discovery

There are dozens of asset allocation models that can provide you with excellent diversification.

They can get you as close to a crisis-proof, inflation-proof hardened wealth plan as you can get.

Some of them come from brilliant financial minds like hedge fund managers Ray Dalio and Rob Arnott.

Many of the models recommend owning a mix of assets like U.S. stocks, non-U.S. stocks, real estate, government bonds, gold, commodities, and private business.

For example…

The “all weather” portfolio allocation model from Arnott recommends a portfolio have 30% in stocks, 40% in bonds, and 30% in “real assets” like commodities and real estate.

And the hardened portfolio allocation model from Dalio recommends a portfolio have 30% in stocks, 55% in bonds, and 15% in real assets.

Another diversified portfolio model, from respected investor Mohamed A. El-Erian, has 51% in stocks, 17% in bonds, and 32% in real assets.

With dozens of models to choose from, what is an investor to do?

I have good news for you…

It turns out, if you get the basic idea of “diversification” right, the fine details don’t matter much.

Our friend Meb Faber is the CEO and Chief Investment Officer of Cambria Investment Management. Meb is a brilliant guy and a master of using computerized analysis to evaluate investment and asset allocation models.

In 2013, Meb performed a comprehensive study of how various asset allocation models have performed over the long term. He studied many of the world’s most highly regarded asset allocation models.

Meb found there isn’t much difference in the long-term results of the best models. Their long-term average annual returns are within about one percentage point of each other. They return 9% to 10% per year with much less volatility than an all-stock portfolio.

This means investors shouldn’t get hung up on whether they have 30% of their wealth in stocks or 35% in stocks. Getting the general vicinity, percentagewise, is what counts.

Meb’s other big discovery concerns fees.

Meb found that the amount of fees investors pay to own investments has huge effects on long-term performance… a much larger impact than the specifics of each model.

That’s right. Meb found that fees, not specific asset mixes, have the largest effect on investor returns.

So, don’t obsess over the fine details and the percentage point of your wealth in stocks vs. bonds.

Instead, focus on driving your investment costs and fees into the basement.

For more on all that, we highly recommend Meb’s book Global Asset Allocation: A Survey of the World’s Top Investment Strategies.

If you’re interested in learning more about the critical importance of keeping your investment fees low or picking a “set it and forget it” asset allocation, Meb’s book is a great resource.

What Category Are You In?

To make the right asset allocation decisions for you, you must first make three decisions:

- What your risk tolerance is,

- What your financial goals are,

- And how long you have to achieve them.

Deciding who you are as an investor is critically important to your wealth plan.

There’s an old saying: “If you don’t know who you are, the market is an expensive place to find out.”

Although we all come from different walks of life, have many different goals, and have various time frames, we at InvestorPlace believe we can all be grouped into one of three investor categories.

See which category best describes you (keeping in mind that these are fictional, hypothetical descriptions of people):

Category #1: The Conservative Investor

The conservative investor is focused on creating a safe investment portfolio they can generate income from.

Meet David and Laura. They are retired, comfortable, and looking to stay that way…

David and Laura are in their 70s.

They are not “super wealthy,” but they have amassed a nice nest egg over their 50-plus years of working, saving, and raising a family. They own their house and have $500,000 in liquid, investable assets.

Their chief concern is not losing a penny of that wealth. Their second concern is earning safe income from it. They want income to supplement their Social Security and pension checks.

This means David and Laura are not interested in taking the risks involved in starting a new business. They are not interested in trading growth stocks in their spare time.

They want to build safe, diversified income streams with bonds, stocks, real estate, and other assets.

David and Laura are focused on safety and income from the portfolio.

You can boil down their desired investment plan to one word: Conservative.

Category #2: The Growth Investor

The growth investor is focused growing their investment portfolio to generate returns over the long term.

Steve and Rachel are in their mid-40s and still working and saving. Their three children are in high school and junior high.

Steve and Rachel make good incomes from their jobs, but they are not “rich.” They also worry about having enough money to send their kids to college, living their ideal lifestyle once the kids are out on their own, and having a comfortable retirement.

They’ve seen research that shows stocks generate high returns over the long term. They have a 20+ year investment time horizon and are comfortable having a good chunk of their investable assets in the stock market.

Steve and Rachel are focused on growing their investment portfolio.

You can boil down their desired investment plan to one word: Growth.

Category #3: The Aggressive Growth Investor

The aggressive growth investor is focused on growing their wealth over a lengthy time horizon and has the ability to take on riskier investments.

Chris is single, has no kids, and is in his late 20s. He’s just getting started on his road to wealth and willing to take risks.

He is on a promising career path… and he’d like to be wealthy someday. He has about $25,000 in savings right now. He’s young and knows that he has decades of working years to make money.

That ability to earn money for a long time could come in handy in case he suffers a loss with an investment or failed business venture.

Chris is willing to take risks in business and with his investments that wouldn’t make sense for someone in their 60s.

Chris is focused on the growth of his net worth… and is willing to take some risks to do that.

You can boil down his desired investment plan to two words: Aggressive Growth.

Source: InvestorPlace.com

Source: InvestorPlace.com

Creating an Asset Allocation Plan to Meet Your Goals

If you don’t perfectly fit into one of the categories above, don’t worry.

Maybe you only have a small amount of capital to invest…

Maybe you are coming up on retirement but are worried you don’t have enough funds to work for you without a regular paycheck…

Maybe you are trying to grow your wealth but also paying off debts…

No matter your current financial situation, if you have capital to invest, an asset allocation model is the best way to protect and grow your wealth…

Again: There’s no way anyone can provide a “one size fits all” asset allocation plan to a large group of people.

Everyone’s financial situation is different.

An asset allocation that will work for one person could be terrible for another person.

For example, someone who is 75 years old should invest much more conservatively than someone who is 30 years old. This means owning more bonds than stocks.

To get an idea of how you should allocate your assets, it’s critical that you decide what category you should be in.

Are you past 70 years old and retired… or close to it?

Then you’re probably in the “Conservative Investor” category.

Are you in your late 30s or mid 40s?

Then you’re probably in the “Growth Investor” category.

Are you in your mid 20s or early 30s?

Then you’re probably in the “Aggressive Growth Investor” category.

While deciding which category best describes you, consider some of these ideas that factor into smart asset allocation:

- Stocks produce superior long-term returns. But they can go through deep and long bear markets.

If you’re younger and more comfortable with the volatility involved in stocks, you can keep a stock exposure to somewhere around 50% to 75% of your portfolio.

A young person who can place a significant chunk of their wealth into stocks and hold them for decades stands to do very well. But they will have to go through some volatile times.

- If you’re older and can’t stand risk or volatility, consider keeping a significant portion of your wealth in cash and bonds… like a 75% to 85% weighting.

Near the end of your career as an investor, you’re more concerned with preserving wealth than growing it, so you want to be very conservative.

When it comes to determining which category you belong to – and what kind of asset allocation mix is right for you – keep in mind your age… your risk tolerance… and your station in life.

Whatever mix you choose, just make sure you’re not overexposed to an unforeseen crash in one particular asset.

This will make your hardened wealth plan as “crisis proof” and “inflation proof” as possible.

Don’t Forget to Rebalance!

Once an investor picks an allocation model, they can “rebalance” it at the end of each year.

For example, say you set your stock allocation at 30%. This is where you aim to keep your stock allocation at all times.

Now let’s say your stock allocation soars in value in a given year while your bond allocation does not soar in value.

This hypothetical increase in value makes it so your stock allocation grows to be 35% or 40% of your portfolio’s value.

In this situation, you’d sell some stocks at the end of the year and buy more of your other allocation groups. This selling of stocks and buying of other groups would “rebalance” your portfolio and get you back to your target allocations.

Summing Up

Stop “Obsessing Over Predictions”… and Get on With Your Life

My favorite part of crisis-proof, inflation-proof “hardened” portfolios is that they go a long way toward getting people out of the “obsessing over predictions” business.

Once you start investing and following the financial news, you’re sure to come across dozens of different financial predictions made by people with impressive credentials.

Some of these predictions will be wildly optimistic… like “DOW 100,000!”

Some of these predictions will be wildly pessimistic… like “Next Great Depression Ahead!”

If you’re a dedicated reader of financial news and research, you’ll come across hundreds of big predictions in a given year. It’s enough to make an amateur investor’s head spin. (It’s also enough to make a longtime professional investor’s head spin.)

I’m in the business of selling investment research… so allow me to take you behind the curtain of the financial industry: We know the louder and more audacious a prediction is, the more people will pay attention to it.

That’s how the world works. That’s why the hundreds of big predictions you hear each year can create brain overload. It can cause people to lose sleep at night, obsessing over something they read online. People can worry themselves straight into “analysis paralysis.”

When you build a crisis-proof, inflation-proof hardened portfolio, you don’t need to worry about the next 15% move in the stock market. You don’t need to worry about rising interest rates. You don’t need to worry bull and bear markets. You don’t need to worry about inflation going up or down.

Of course, these things can affect the value of your portfolio in the short term, but you can sleep easy at night knowing you have a robust, diversified portfolio that safely grows in value over time… through bear markets, wars, bull markets, booms, recessions, crashes, and all the rest.

Sitting on top of your hardened portfolio, you may wish to entertain wildly optimistic and wildly pessimistic predictions. You may wish to spend hours reading detailed forecasts or watching financial news.

But you can do it for entertainment and education… and not in the pursuit of worrying or frantically trading in and out of stocks.

You can get out of the obsessing over predictions business and get on with your life.

When your portfolio is as safe and as hardened as the Cheyenne Mountain Complex, you don’t worry about the weather.

Regards,

Brian Hunt

CEO, InvestorPlace

The post How to Build a Crisis-Proof, Inflation-Proof Portfolio appeared first on InvestorPlace.