Uncategorized

Weekly Wrap: Local and Global markets, Gold prices, Inflation, Energy, Tech Stocks & Bond Yields Just a Hot Mess

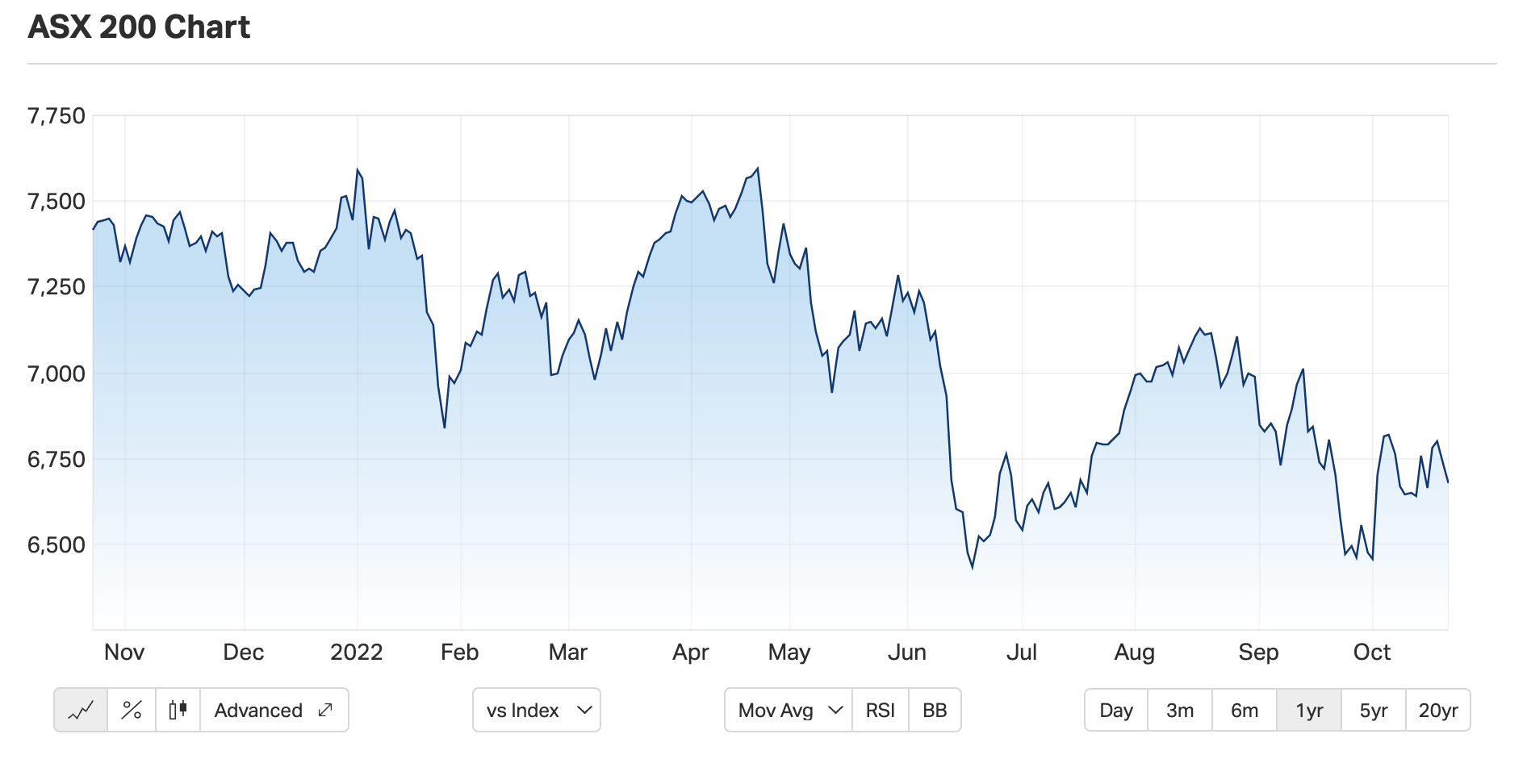

ASX 200 down on 0.8% Friday, ends week just 0.5% higher. The small cap index up 0.2% up 1.4%. And local … Read More

The post Weekly Everything Wrap:…

- ASX 200 down on 0.8% Friday, ends week just 0.5% higher

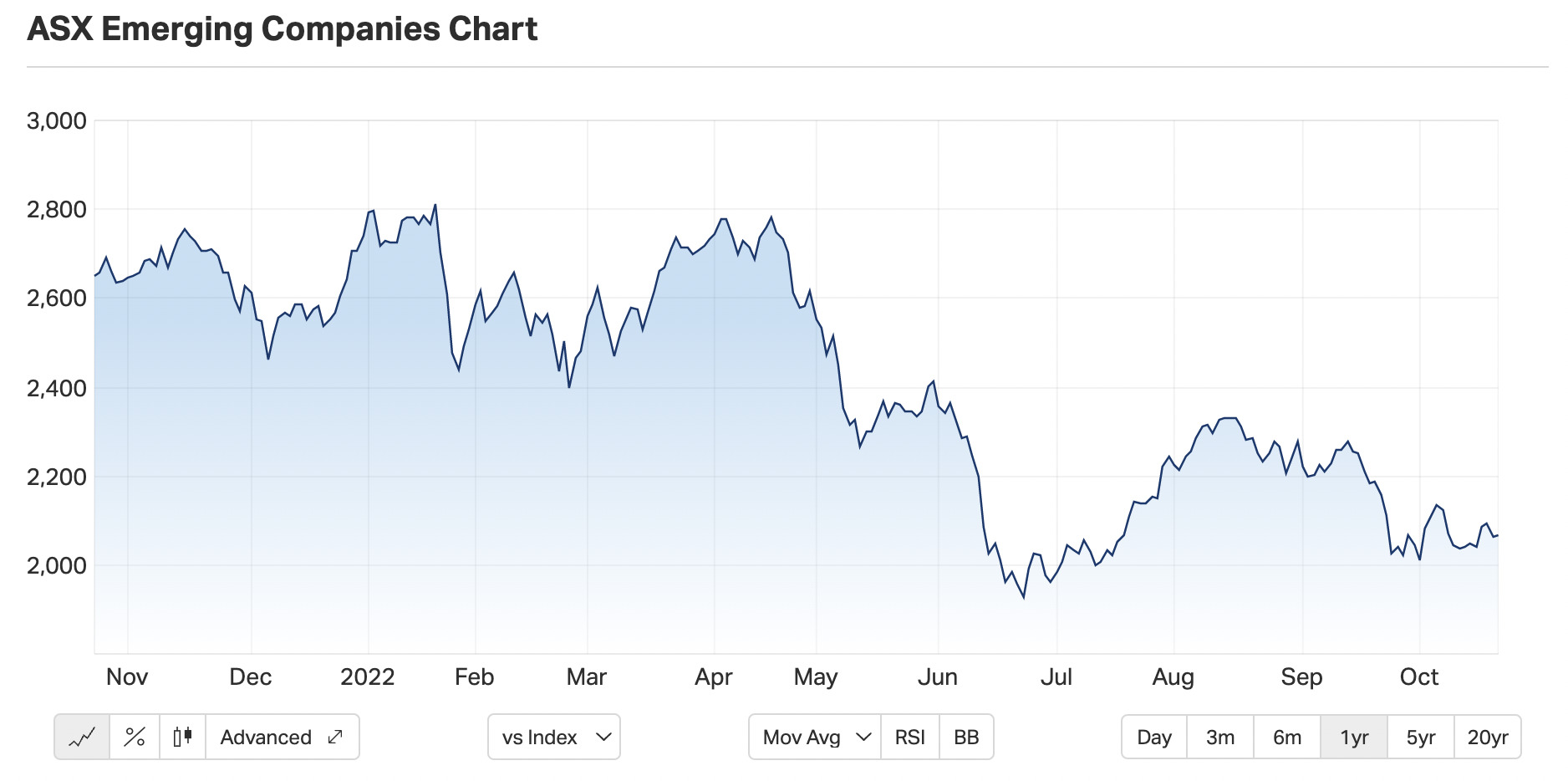

- The small cap index up 1.4%

- Local Toys’R’Us ANZ done good, up 130%

Global markets have been all tippy-toes again this week amid ongoing fears of inflation and interest rates, China’s 20th National Party Congress, war escalating in Ukraine, the UK losing its PM and so very, very much more.

The ASX 200 benchmark has ended a volatile mess of a week 0.5% higher.

The small caps (XEC) index has ended the week 1.4% higher.

At home the October RBA meeting meetings kicked off the week’s information flow.

Westpac’s chief rates economist Bill Evans thought the minutes were pretty exciting in their granular presentation of the back and forth as Dr P Lowe’s crew assessed the case for hiking 25bps (their eventual decision) and 50bps (the market’s prior expectation) at the October meet.

“Arguing for 50bps were inflation and wage risks, particularly while the economy remains strong; the cash rate not being especially high; and the potential for the market and/or community to question the resolve of the Board.”

In favour of a 25bp hike however, was recognition that downside risks to activity growth are building; that inflation could subside quickly; and also the lag between the change in policy and its impact. Also clear from the minutes was that reducing the pace of hiking to 25bps per month is not a sign of a near-term pause, with “further increases in interest rates over the period ahead” expected.

That gave shares at home another champagne pop to begin the week which fell quickly flat and unneffervescent as inflation, recession, depression, the continuing rise in bond yields and the rate rises which bully them in charge for the rest of the week. The All Ords fell as materials, health, utility and industrials more than offset gains in property and energy stocks.

Dr Shane Oliver, my Friday friend in fiscal fact checking, said it’s been more of the same for investment markets. The yield on 2-Year US Treasury notes rose to 4.61% and the yield on the 10-Year US Treasury notes rose to 4.23%.

“Shares have managed yet another bounce from technical support levels for US shares, and extremely bearish investor sentiment and oversold conditions suggest that they may have more upside.”

This is the volatile pattern which also left US and Eurozone shares up but Japanese and Chinese shares down.

Bond yields fell in the UK as the 23rd September fiscal stimulus was largely reversed, but rose elsewhere with the US 10-year bond yield rising to its highest since 2007.

Iron ore was up 1.6% in Singers, but the neighbouring Asian markets were all lower, Japan’s Nikkei gave away 4%, while Hong Kong’s Hang Seng continues to depress anyone who is rooting for that once great city-state. Fresh off a 13-year low, the Hang Seng still found the energy to shed another circa 0.2% .

Mainland China markets in Shanghai and Shenzhen, ashamed to be a part of a really ugly week in post-Hu Jintao transparency, were neither here nor there and you wouldn’t trust them if they went another way.

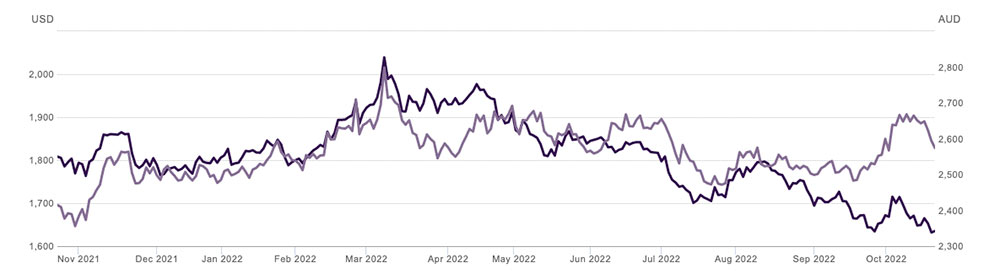

Gold fell 0.5% at $US1621/oz.

Reuben, digging around the formerly safe haven for evidence of some kind of deeper meaning sought answers from experts he knows are probably more confused than US President Joe Biden.

“Gold has been the unexpected loser of the current macroeconomic environment, with its safe-haven status in direct competition with the U.S. dollar,” said Aude Marjolin, associate commodity analyst at S&P Global Commodity Insight.

The likely culprits, Reuben reckons, would be the geopolitical volatility – gold briefly hit $US2,000oz in March after Russia invaded Ukraine – and the loopy things The Fed is doing to the greenback, which appears to have been exposed to Gamma radiation.

The muscular US currency is being a real bugbear for a Fed trying to be tough in its monetary policy battle vs inflation.

Historically, strong dollar = weak gold price, and vice versa.

So, what could boost the gold price? A loosening of monetary policy.

“I tend to think that Fed hawkishness is largely now ‘in the price’,” Philip Klapwijk, managing director of Hong Kong-based consultant Precious Metals Insights told livemint in an email. “That said, the scope for a near-term major rebound in gold prices is very limited while rates climb and the US dollar remains strong.”

More annoyingly: more red herring-smelling data at home. Jobs this time. And they subsequently surprised to the downside, a deep downside – we were expecting circa 25K, we created 900 created last month.

While WBC’s economics team expect employment growth to “remain robust into 2023,” an improving population growth should also “limit further downside for the unemployment rate,” and help to better match labour supply and demand.

Further afield, lots of big central banks are expected to once more unto the breach hoist their interest rate petards.

Germany and The Canadians come to mind as two looming petard hoisters – the global price pressures continue to make my usually gripping visit to Fruit World a dull experience.

Anarchy in the UK

Yes, the British Prime Minister Liz Truss will be calling it a day (or about 6 weeks) and will step down as soon as the world’s worst political party (at least the Chinese Communists just cancel their bad numbers) the UK Conservatives go and get another one – about a week, extending her stay in Downing St by about 14%. While undeniably action-packed – Truss laid to rest Queen Elizabeth II and a week later almost laid to rest the unsinkable reputation of the British Pound – hers will untrouble historians as the briefest, certainly the dumbest term of any Brit Prime Minister in history.

Wait. There is one man who might challenge for the title of Britain’s not got talent, which is why there’s already speculation Truss’s predecessor Boris Johnson could put up his hand. You probably didn’t hear that here first, but considering the man’s passion for attention and melodrama I’m going to put my own hand up and say he’ll be exhumed and back in number 10, reeking of mud and shame and delight by November.

The drone war we had to have

We’ll get more into this next week, but Stockhead spoke at length with Droneshield boss Oleg Vornik after a major capital cities across Ukraine (and on the European continent) were attacked en masse by suicide bombing drones made in Iran.

Kiev claims to have shot down 13 of the 24 drones launched on October 10, as well as the 13 launched the following day, a claim which cannot be verified at this stage.

Oleg says the Iranian drone tech may even have been first sighted in the Ukraine theatre as early as August, but this week’s unprecedented wave upon wave of swarm attacks, in which office blocks tumble and civilians die, is most definitely new.

But it’s the swarm strikes on civilian centres in Europe which is new to this war, new in fact to all war and the clear success of the cheap (think US$20k per drone vs $1m per Russian strike missile) and accessible systems will ensure swarming UAV attacks and other forms of drone tech will make it a handy go-to option of all sides in all the new wars to come.

“I think there’s a number of thresholds crossed this week. Not least the first Western country attack using drone warfare,” Vornick says.

“We have seen similar (but less reported) situations in Middle East (Houthi drone attacks on Saudi, including on Riyadh itself; Syria, Armenia/Azerbaijan etc).

“When we set up the business 8 years ago, we believed that drone technology was going to rapidly evolve (like any technology), and as such ‘democratise’ the warfare – with drones in war previously limited to only a few countries who could afford to develop and buy larger drones.”

At this point, drones are everywhere – suicide attacks, dropping charges, directing artillery fire, scoping out battlefield intel etc. While they alone do not decide the course of war, they are a part of the combined arms concept, meaning being used in tandem with other parts of the military (such as artillery).

Iranian-made drones have been used elsewhere in Ukraine in recent weeks against urban centres and infrastructure, including power stations. Half of Ukraine is already in blackout.

And at a relative steal the Shahed (or martyr in Farsi) is a revolution in the cheap urban war stakes.

Compared to the cost of cutting-edge missiles, precision strike weaponry, conventional aircraft, the pilots to fly them… why bother with any of that when killing and terrorizing civilians actually is your goal?

This will make you feel better, turn up the volume.

Rocking DroneShield 2021 Corporate Vid Via DroneShield on Vimeo.

Petard hoisting and goose cooking

Many clever people said this week inflation is already a cooked goose. I’m not sure that’s clarified much for me. There seems to be many geese and they’re all still flying about willy nilly according to the Fruit World test.

Legendary thinker, meanwhile, Stephen The Kouk Koukoulas, is most definfitely of the hoisted by their own petard* school of legendary thought:

ICYMI

The labour market has started to soften and let’s hope the RBA doesn’t keep hiking when higher unemployment is already in the bag. https://t.co/hf4zyZpCBD— Stephen Koukoulas (@TheKouk) October 20, 2022

To be “hoist by [or with] your own petard” is to be blown up by your own bomb. A petard was a medieval engine of war consisting originally of a bell-shaped metal container filled with explosives. It was used to blow in a door or a gate or breach a wall. Premature explosion was an ever-present danger. In other words, you could be hoist by your own petard. But what is also interesting is the derivation of the word “petard”. It comes from the French word peter, meaning to fart. The French are both lovely and gross.

Of course, and I’m almost done, to be “hoist with his own petar” is to be blown up by your own bomb (as in Hamlet, Act III, Scene IV, where Hamlet refers to Polonius being destroyed by his own plotting) so it basically means being instead hurt… by one’s own action intended to harm another. And it ain’t no flagpole, but you’ve probs got the full answer to an unwanted question.

Inflation data in the UK and Canada came in above expectations this week. That’s probably more prescient.

Germany’s producer prices rose strongly in September from a year earlier, driven by higher energy prices, the German statistics office Destatis said.

In commodity markets, Brent crude oil gained 0.1% to US$92.49 a barrel.

In local bond markets, the yield on Australian 2-Year government bonds rose to 3.50% while the 10-Year rose to 4.05%.

Oil prices rose this week topping to $US93 a barrel as caution over tightening supply in the wake of OPEC+ truculence offset the negative impact of uncertain demand and news that the US will release more crude from its reserves.

5 UP:

(6 actually) ASX stocks which have made straight gains in last five or more sessions

Origin Energy said it expects earnings from its core energy supply business to jump as much as 78% this financial year in a recovery from last year’s slump, boosted by increases in profits from sales of gas, while electricity profits remain “suppressed”.

At home, the twins were up to much good. Woodside delivered record quarterly production of 51.2M barrels of oil equivalent in the September quarter, up 52% from the previous quarter, while revenue hit a record of $5.9b, up 70% from Q2. Strong gas prices propelled Santos to record sales of $US2.15b in the September quarter, up 15% on the June quarter.

Things you didn’t know

Another incredibly promising Indian unicorn – Desi logistic giant Delhivery’s – has been delivered 48 hours of despair as its share price went into an expensive fall, crashing to an all time low over the last two sessions.

Since Thursday morning, the tech logistics play has yielded up some 30% on little worse than a muted growth outlook. Delhivery’s shares tanked 15% on the BSE, finding further frailty on Friday with a follow-up 15% fall.

Zomato looking at #Delhivery pic.twitter.com/5f0A1xslow

— Shreejon Biyani (@ShreejonBiyani) October 21, 2022

Alliteration aside, Delhivery stocks have now tracked some 20% lower than its headline IPO earlier this year.

The firm joins former heroes of the dish Zomato and Paytm in the market slump that’s made a mockery of the world-beating generation of Indian new-age tech.

Next Week

- In Australia, the focus will be on the Tuesday Budget

- CPI and trimmed mean inflation are expected to rise to their highest since 1990, in line with RBA forecasts (consistent with another 0.25% rate hike in November, according to AMP Capital)

- Producer price inflation for the September quarter will also be released on Friday. October business conditions PMIs (Monday)

- US, September quarter GDP (Thursday) is expected to rise

- US October business conditions PMIs (Monday) to remain softish

- US home prices and consumer confidence are expected to fall (Tuesday) as are home sales data

- September core private final consumption deflator inflation is expected to rise

- US The September quarter earnings reporting season will continue.

- Bank of Canada (Wednesday) likely to hike rates by another 0.75% taking its official rate to 4%.

- The ECB (Thursday) is expected to raise its key policy rates by another 0.75%

- EU business condition PMIs for October (Monday) and economic confidence (Friday) are expected to soften further.

- The Bank of Japan (Friday) is expected to leave unchanged is ultra easy monetary policy

- Japanese business conditions PMIs for October (Monday) and jobs data (Friday) will also be released.

- Delayed Chinese data may get released, but …

ASX IPOs

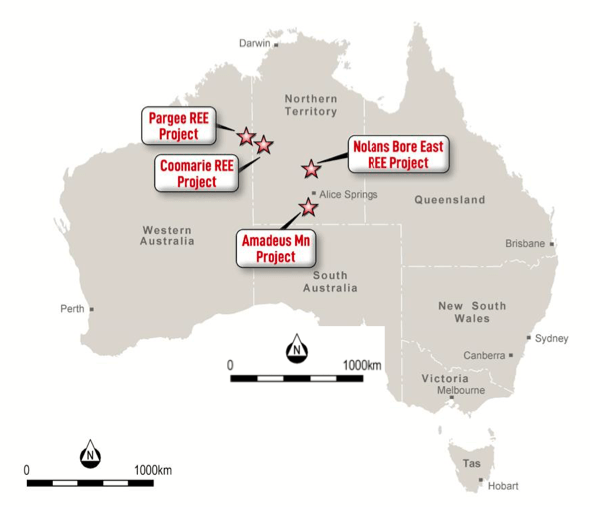

Bubalus Resources (ASX:BUS) listed last week after a $5m IPO at $0.20 per share.

This explorer is focused on the exploration and development of manganese and rare earths projects in the NT and WA.

Projects include the Amadeus Project (prospective for manganese), the Coomarie Project (prospective for Heavy Rare Earths), the Nolans East Project (prospective for Light Rare Earths) and the Pargee Project (prospective for Heavy Rare Earths).

The company peaked at $0.25 after listing, before settling down at $0.23 per share at COB yesterday.

Who is listing this week?

Listing: 21 October

IPO: $15m at $0.20

This O&G junior has two exploration permits in the Surat Basin in South East Queensland, ATP 2037 and ATP 2038. The two permits represent an area of over 250,000 acres and are located approximately 50km away from critical gas transmission infrastructure.

And it looks like gas investment is heating up in Queensland. Just last week QLD-focused State Gas (ASX:GAS) attracted a $7 million investment from leading energy sector experts St Baker, headed by Trevor St Baker – who recently chatted with Stockhead’s Bevis Yeo.

Omega’s exploration program will explore the Permian Deep Gas play which, if successful, represents a potential multi-TCF gas resource.

Australia Sunny Glass Group (ASX:AG1)

Listing: possibly…

IPO: $7.5m at $0.35

This Australian-based holding company, through its subsidiaries, operates a glass production and supply business for structural building facades.

The group has a fully automated processing plant which it says is highly-efficient, accurate and scalable and an R&D focus on the development of cyclone resistant glass using new laminating and bonding techniques.

These are the companies Emma reckons might be listing in the next week

Nightingale Intelligent Systems (ASX:NGL)

Listing: 24 October

IPO: $10m at $0.35

This company develops and sells Unmanned Aerial Vehicles (UAVs) or drones for commercial applications – and there’s a bunch of them.

NGL says its tech has applications across solar farms, ports, O&G facilities, critical infrastructure like dams and power stations, in construction, border patrol, securing pipelines, fire and oil spills along with search and rescue, crowd control and for prisons.

Basically, the drones can respond to a threat; when a security alarm is triggered the system automatically dispatches a drone to the alarm location and streams live video to the security team.

Listing: 24 October

IPO: $32.5m at $0.20

This resources player is focused on developing a gold platform in West Africa.

The company is primarily focused on the development of the Kobada Gold Project in Southern Mali, which has a global resource base of over 2.3 Moz of gold and the potential to produce more than 100,000 ounces of gold per annum.

Listing: 25 October

IPO: $30m

This investment company says it’s focused on risk adjusted returns through constructing a high conviction portfolio of 20-25 microcap ASX-listed companies.

Listing: 26 October

IPO: $55m at $1.46

This natural gas player is focused on the shallow waters offshore Indonesia, and via its wholly owned subsidiaries is the holder of several operated tenements in offshore Indonesia in the form of Production Sharing Contracts (PSCs) with Duyung PSC (76.5% interest) and Offshore Mangkalihat PSC (100% interest).

The company has also completed joint studies in two areas in Offshore North West Aceh and Offshore South West Aceh in the offshore Aceh Province in Indonesia, and will have the right to match in the bidding process for both areas when they are gazetted as PSCs in a future licensing round.

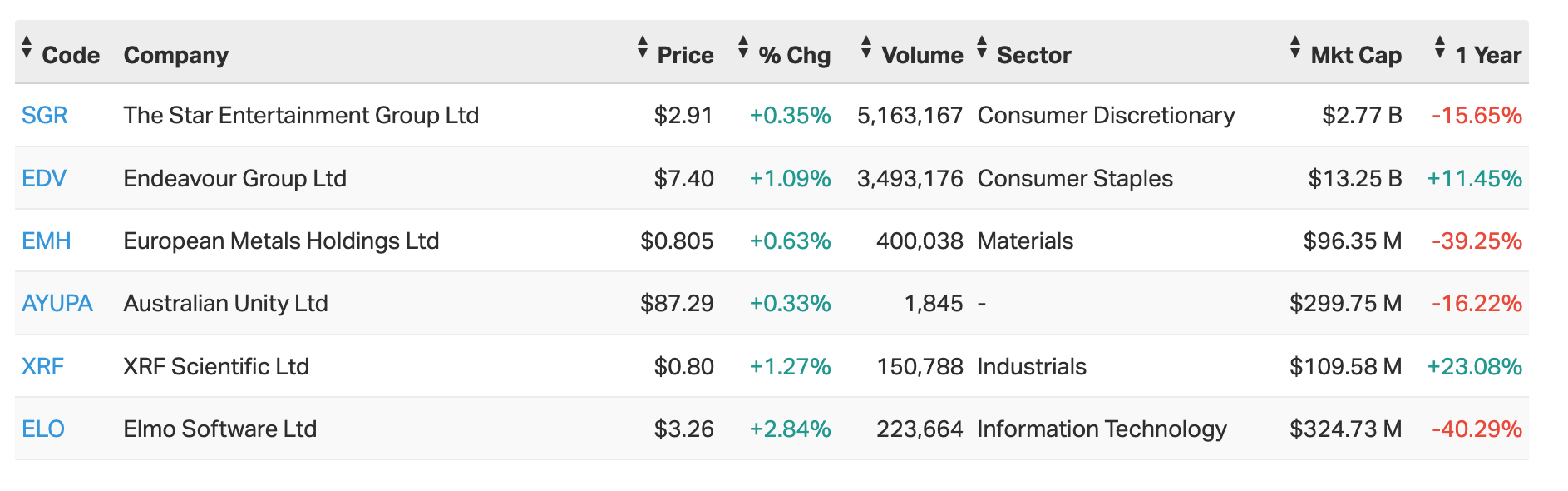

ASX SMALL CAP LEADERS:

Here are the best performing ASX small cap stocks for September 24 to September 30:

Swipe or scroll to reveal full table. Click headings to sort:

| Code | Company | Price | % Week | Market Cap |

|---|---|---|---|---|

| TOY | Toys R Us | 0.056 | 133% | $53,435,393 |

| 1CG | One Click Group Ltd | 0.02 | 67% | $10,671,444 |

| DEL | Delorean Corporation | 0.11 | 67% | $23,729,301 |

| STK | Strickland Metals | 0.053 | 51% | $63,593,559 |

| MEB | Medibio Limited | 0.0015 | 50% | $4,980,891 |

| TD1 | Tali Digital Limited | 0.003 | 50% | $3,697,892 |

| HPC | Thehydration | 0.155 | 48% | $22,297,658 |

| MAY | Melbana Energy Ltd | 0.09 | 48% | $296,577,961 |

| JXT | Jaxstaltd | 0.025 | 47% | $8,564,455 |

| BTN | Butn Limited | 0.1875 | 39% | $13,322,711 |

| LVE | Love Group Global | 0.1 | 39% | $2,918,460 |

| ADY | Admiralty Resources. | 0.008 | 33% | $9,125,054 |

| AO1 | Assetowl Limited | 0.002 | 33% | $3,144,260 |

| CFO | Cfoam Limited | 0.004 | 33% | $2,935,363 |

| GGX | Gas2Grid Limited | 0.002 | 33% | $8,116,204 |

| RR1 | Reach Resources Ltd | 0.006 | 33% | $11,460,304 |

| VTI | Vision Tech Inc | 0.265 | 33% | $6,642,403 |

| MMG | Monger Gold Ltd | 0.48 | 32% | $19,219,200 |

| PPL | Pureprofile Ltd | 0.036 | 29% | $38,745,794 |

| TAS | Tasman Resources Ltd | 0.018 | 29% | $11,409,594 |

| TGM | Theta Gold Mines Ltd | 0.082 | 28% | $48,118,580 |

| NVX | Novonix Limited | 2.265 | 28% | $1,109,630,181 |

| PEK | Peak Rare Earths Ltd | 0.465 | 27% | $104,711,011 |

| MRL | Mayur Resources Ltd | 0.165 | 27% | $39,919,689 |

| BUR | Burleyminerals | 0.17 | 26% | $5,834,918 |

| SXG | Southern Cross Gold | 0.37 | 25% | $21,791,963 |

| AMD | Arrow Minerals | 0.005 | 25% | $10,168,825 |

| DLT | Delta Drone Intl Ltd | 0.015 | 25% | $4,498,295 |

| FOD | The Food Revolution | 0.03 | 25% | $28,402,850 |

| PG1 | Pearl Global Ltd | 0.0225 | 25% | $22,550,565 |

| SEN | Senetas Corporation | 0.03 | 25% | $33,986,278 |

| ACW | Actinogen Medical | 0.125 | 25% | $224,486,727 |

| E25 | Element 25 Ltd | 1.12 | 24% | $171,799,165 |

| R3D | R3D Resources Ltd | 0.099 | 24% | $10,803,386 |

| ONE | Oneview Healthcare | 0.16 | 23% | $80,598,513 |

| IMB | Intelligent Monitor | 0.092 | 23% | $12,024,427 |

| REC | Rechargemetals | 0.19 | 23% | $7,561,050 |

| NCR | Nucoal Resources Ltd | 0.011 | 22% | $8,454,736 |

| AZS | Azure Minerals | 0.275 | 22% | $85,452,323 |

| SYR | Syrah Resources | 2.065 | 22% | $1,394,787,077 |

| GEN | Genmin | 0.25 | 22% | $70,821,963 |

| ACR | Acrux Limited | 0.073 | 22% | $20,840,757 |

| RNU | Renascor Res Ltd | 0.23 | 21% | $467,344,434 |

| AS2 | Askarimetalslimited | 0.47 | 21% | $21,375,187 |

| XTE | Xtek Limited | 0.56 | 20% | $54,442,511 |

| XRF | XRF Scientific | 0.8 | 20% | $108,214,812 |

| ADR | Adherium Ltd | 0.006 | 20% | $15,371,099 |

| COY | Coppermoly Limited | 0.012 | 20% | $26,327,483 |

| ICE | Icetana Limited | 0.048 | 20% | $8,969,779 |

| MYG | Mayfield Group Ltd | 0.3 | 20% | $27,175,768 |

It’s all fun and games until you realise you never bought TOY stocks.

Toys’R’Us ANZ (ASX:TOY) began rising early in the week and never stopped. It was only later in the piece that the former furniture-named business has signed a cracker of a deal to trial nine Toys’R’Us store-in-store implants in the United Kingdom.

TOY penned an exclusive sub-licence agreement with WH Smith High Street, with the implants scheduled to open in the first half of 2023.

The company reported the UK market represents a significant near-term growth opportunity, allowing it to access the largest toy market in Europe and the fourth largest globally.

The trial period begins upon the opening of the first implant and extends for 12 months, and will include the sale of toys, games and children related products typically sold by Toys’R’Us.

ASX SMALL CAP LAGGARDS:

Here are the best performing ASX small cap stocks for September 19 to September 23:

Swipe or scroll to reveal full table. Click headings to sort:

| Code | Company | Price | % Week | Market Cap |

|---|---|---|---|---|

| MRR | Minrex Resources Ltd | 0.045 | -18% | $46,578,286 |

| RAD | Radiopharm | 0.13 | -18% | $16,884,100 |

| QXR | Qx Resources Limited | 0.066 | -19% | $58,202,913 |

| AUH | Austchina Holdings | 0.0065 | -19% | $13,239,413 |

| EMT | Emetals Limited | 0.013 | -19% | $11,900,000 |

| SRX | Sierra Rutile | 0.2025 | -19% | $89,089,654 |

| AMS | Atomos | 0.1025 | -20% | $23,346,916 |

| EYE | Nova EYE Medical Ltd | 0.225 | -20% | $37,195,434 |

| 99L | 99 Loyalty Ltd. | 0.024 | -20% | $27,832,386 |

| CPT | Cipherpoint Limited | 0.004 | -20% | $3,316,653 |

| GES | Genesis Resources | 0.008 | -20% | $6,262,730 |

| GSR | Greenstone Resources | 0.024 | -20% | $26,393,849 |

| KFE | Kogi Iron Ltd | 0.004 | -20% | $6,528,311 |

| MGG | Mogul Games Grp Ltd | 0.002 | -20% | $6,526,882 |

| MTB | Mount Burgess Mining | 0.004 | -20% | $4,295,856 |

| NGY | Nuenergy Gas Ltd | 0.024 | -20% | $35,542,932 |

| PVL | Powerhouse Ven Ltd | 0.052 | -20% | $6,278,645 |

| SYN | Synergia Energy Ltd | 0.002 | -20% | $16,835,581 |

| TSC | Twenty Seven Co. Ltd | 0.002 | -20% | $10,643,256 |

| MP1 | Megaport Limited | 6.06 | -21% | $922,102,620 |

| RXL | Rox Resources | 0.19 | -21% | $32,098,780 |

| OLY | Olympio Metals Ltd | 0.15 | -21% | $6,852,874 |

| OSX | Osteopore Limited | 0.2 | -22% | $26,971,695 |

| CNJ | Conico Ltd | 0.014 | -22% | $20,369,554 |

| CYQ | Cycliq Group Ltd | 0.007 | -22% | $2,432,617 |

| EX1 | Exopharm Limited | 0.105 | -22% | $16,507,211 |

| AJL | AJ Lucas Group | 0.066 | -22% | $112,809,830 |

| TNG | TNG Limited | 0.07 | -23% | $102,742,948 |

| MCM | Mc Mining Ltd | 0.23 | -23% | $45,460,620 |

| PNR | Pantoro Limited | 0.1375 | -24% | $267,964,518 |

| TG1 | Techgen Metals Ltd | 0.11 | -24% | $6,022,385 |

| MYE | Metarock Group Ltd | 0.25 | -24% | $29,473,323 |

| NRX | Noronex Limited | 0.028 | -24% | $4,772,874 |

| AHI | Adv Human Imag Ltd | 0.098 | -25% | $17,666,185 |

| ANR | Anatara Ls Ltd | 0.045 | -25% | $3,282,359 |

| CAD | Caeneus Minerals | 0.003 | -25% | $18,709,618 |

| DDDDB | 3D Resources Limited | 0.0075 | -25% | $3,545,498 |

| NZS | New Zealand Coastal | 0.003 | -25% | $3,944,518 |

| PUA | Peak Minerals Ltd | 0.006 | -25% | $6,248,225 |

| SHO | Sportshero Ltd | 0.021 | -25% | $11,965,682 |

| WBE | Whitebark Energy | 0.0015 | -25% | $9,697,329 |

| Z2U | Zoom2Utechnologies | 0.1 | -26% | $13,153,668 |

| DW8 | DW8 Limited | 0.004 | -27% | $11,200,181 |

| KP2 | Kore Potash PLC | 0.012 | -29% | $7,521,389 |

| GME | GME Resources Ltd | 0.088 | -32% | $55,898,047 |

| JAV | Javelin Minerals Ltd | 0.001 | -33% | $9,454,153 |

| SIH | Sihayo Gold Limited | 0.002 | -33% | $12,204,256 |

| YPB | YPB Group Ltd | 0.004 | -33% | $1,626,185 |

| WWG | Wisewaygroupltd | 0.055 | -35% | $9,201,163 |

| YRL | Yandal Resources | 0.1 | -37% | $11,609,155 |

The post Weekly Everything Wrap: Toys R Us; Local and global markets, UK politics, EU geopolitics, Gold prices, Inflation, Energy, Tech stocks and bond yields just a hot mess appeared first on Stockhead.